You can now acquire more of Tuleva’s membership capital

Tuleva members have a new opportunity to participate even more in Tuleva’s growth: we can transfer membership capital to each other.

We don’t choose between low fees, growth and owners’ profit

Tuleva was founded by people who wanted better pension funds for themselves and were ready to invest both money and time to achieve this. Our mission is to help people build capital efficiently and with confidence. In our first nine years of operation, we’ve been very successful in delivering on that mission: the volume of our fund assets has grown from zero to 1.2 billion euros. More than 80,000 people in Estonia are investing with us.

Our aim is to build a sustainable and profitable business – not a quick exit for the founders. But a sustainable venture can’t run on goodwill alone. Tuleva’s advantage isn’t just low fees, but a unique business model that lets us keep fees low and still be profitable.

So the choice between growth, lowering fees and increasing profits is really a pseudo-choice. Our low fees are part of our product, which helps drive growth. We’ve proven that it’s possible to scale low-fee funds while keeping operating costs low: by assets, we have the largest pillar III fund and the second largest pillar II fund in Estonia.

The graph shows the annual growth of Tuleva Fondid AS’s assets. Data from Pensionikeskus and Tuleva’s own calculations.

It’s not just the rapid growth in the early years that matters, but that growth also continues when volumes are high. New contributions and investors bring growth of around 30% each year. Higher asset volumes mean lower costs. Lower costs mean better long-term returns, i.e. a better product. And that, in turn, fuels new growth. This is the foundation of a successful asset management company.

No one can guarantee that we’ll continue growing at the same pace. At the same time, we have sufficient growth potential. Only 10% of pillar II assets are currently managed by Tuleva’s funds, and only 1 in 5 wage earners invests in pillar III – and even they contribute just 4–5% of their wages on average (1).

Sustainable growth ensures lower fees, new investment growth, and returns to owners at the same time.

Tuleva’s membership capital as an investment

When we founded Tuleva, we agreed on some rules to make sure the interests of owners and investors are aligned. That’s why we believe Tuleva’s membership capital is a worthwhile investment.

First, the capital we raised was never meant to be spent. In the start-up world, there’s a common term, ‘runway’, which refers to how many months the most recently raised capital will last to cover current losses. Our runway has always been infinitely long – in other words, our business has had to sustain itself. The capital raised is meant to meet regulatory prudential requirements and is invested in our own pension fund units, which earn global market returns.

Second, we’ve agreed that each year, 0.05% of our asset volume goes to the association’s members as profit – our funds business pays 0.05% of asset volume to the association annually as a fee. This year, the management company will pay a fee of around 0.6 million euros to the association.

In 2024, the management company’s operating profit was approximately 407 thousand euros, and our membership capital earned around 1.53 millioneuros in financial income.

Thus, the Tuleva association’s membership capital generates income from two sources:

return on investment;

the operating profit of the management company and the association.

We decide on dividend payments every five years, in line with the association’s articles of association. So far, we’ve left profits to grow, which has increased the value of membership capital.

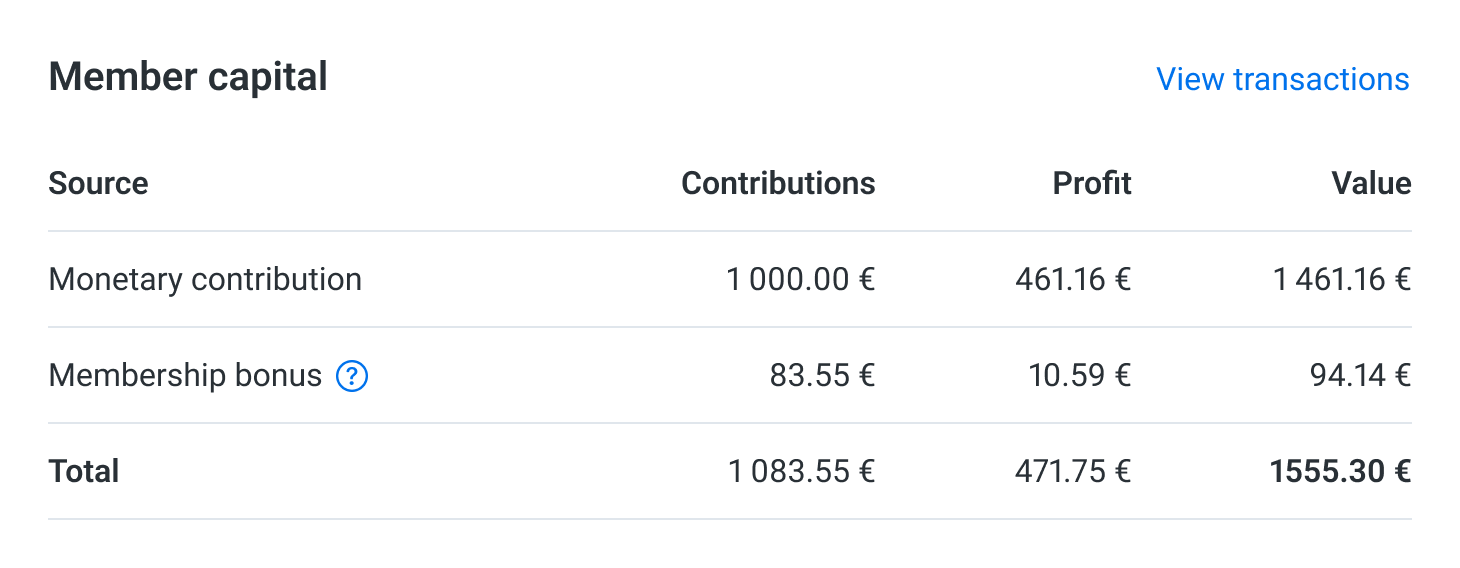

The 1,000-euro membership capital contributed to the Tuleva association in 2016 had a book value of 1,853 euros at the end of 2024.

The membership capital buy-sell solution is available now

We’ve raised capital from the association’s members on two occasions: to launch pillar II funds in 2016 and pillar III funds in 2019. We haven’t needed to raise more capital, though many have asked how they could increase their share in our mutual company.

Now we’ve created a new option. In the spring, at our annual general meeting, we decided to amend the association’s articles of association to give members the option to transfer membership capital to each other. Based on this, the council approved a new membership capital procedure (in Estonian), and we also built a simple technical solution to carry out the transactions. So now, anyone who wishes can:

increase their capital in the Tuleva association;

realise all or part of their capital while still remaining a member of the association.

Tuleva’s membership capital isn’t a security, so buying and selling it works differently from, say, transactions with stocks.

How does the buy-sell process work?

You can see the status of your membership capital by logging in to Tuleva’s web. There are three ways in which a member may have acquired a share in Tuleva’s membership capital:

a voluntary financial contribution made in 2016 and/or 2019 to help launch the Tuleva funds;

an accrued membership bonus; and

a work contribution earned.

After logging in, the association’s members can see a membership capital notice board where they can post their wish to buy or sell membership capital. The buy-sell process works like this:

Log in and add your buy or sell listing to the notice board. Your name won’t be visible in the listing.

If you see a listing that interests you, you can notify the poster through the system, which will send them an email.

You and the other party can agree on the transaction details (price, quantity, payment method, etc.) by email or any other form of direct communication. Tuleva won’t interfere in this.

The seller initiates the membership capital’s transfer application in Tuleva’s web, which both parties need to sign digitally. The buyer transfers the agreed amount to the seller, who then confirms receipt. When reviewing the applications, we’ll automatically check that the requirements are met (both parties are members, the seller has the stated membership capital, the 10% limit isn’t exceeded).

Tuleva’s management board approves the application within a week. Finally, we record the transaction in the register of membership capital and both parties receive a letter confirming it.

Of course, you might also find a member interested in the transaction in some other way. For example, a friend might tell you they want to realise their membership capital. In that case, you can jump straight to step 3.

Frequently asked questions

1. Does buy-sell mean that the previously widely dispersed shareholding will be concentrated in the hands of a few members?

No. First, Tuleva’s membership capital is very widely dispersed – nearly 2,600 members have made membership contributions, and nearly 8,000 have earned membership bonuses. The ten members with the largest shares each hold only 0.75% of Tuleva’s membership capital on average.

Tuleva belongs to 9,000 members, each owning a small piece.

Second, the articles of association set a limit on acquiring Tuleva’s membership capital: an individual member may not own more than 10% of the membership capital contributions.

Third, based on our experience so far, Tuleva’s members generally want to keep their share, so it’s unlikely that a large number of members would wish to sell their membership capital.

2. How is income from the sale of membership capital taxed?

Buying and selling membership capital is a transaction between individual members. Therefore, it’s the member’s personal tax liability, which must be declared in the next year’s income tax return (by 30 April). Contributions made by the member and the cost of acquiring the membership capital are deducted from the acquisition cost. We’ve explained the tax rules in more detail in a separate guide.

3. Why don’t we recommend selling membership capital below book value?

The book value is the amount a member would be entitled to receive as a severance payment if they left the association. In that case, the association pays the severance payment and withholds corporate income tax on the share of profits earned. For this reason, it’s not reasonable to sell your share below book value.

4. How can I find out at what price other members have transferred their membership capital?

We’ll start publishing quarterly aggregated statistics showing the number of transactions and the average transaction price expressed as a multiple of book value. This data will be published for the first time in three months, i.e. in mid-December.

(1) Statistics of the Ministry of Finance 2024

A new option to acquire Tuleva’s membership capital

Starting on 28 April, Tuleva members could vote at the Tuleva association’s general meeting, where we also amended our articles of association. The most important change was the addition of a new option for members to acquire and transfer membership capital between each other.

We’re not an ordinary pension fund. Tuleva is owned by the investors themselves – people who chose to cut out the middlemen and build better pension funds for themselves. We make all the important decisions at general meetings, where each of Tuleva’s nearly 9,000 members has an equal vote. Collective action has served us well and that’s not going to change.

Tuleva members own our membership capital, and profits are distributed based on each member’s share in it. The membership capital is part of the association’s equity, which is fully invested in Tuleva’s management company and earns returns from its operations. While everyone has equal voting rights, each member’s amount of membership capital varies depending on how much they’ve contributed to Tuleva.

You can see the status of your membership capital by logging in to Tuleva’s web application. There are three ways to acquire a share in Tuleva’s membership capital: 1) a voluntary financial contribution made by the member in 2016 and/or 2019 to help launch the Tuleva funds; 2) an accrued membership bonus, earned annually by all members who invest in Tuleva, equal to 0.05% of the value of their pension assets; 3) a work contribution (for Tuleva employees and service providers under option agreements).

How can you acquire more membership capital?

As a Tuleva member, you gradually build up membership capital each year through the membership bonus, as long as you have assets in our pillar II and III pension funds. But what if you’d like to acquire more capital faster?

Normally, you become an owner in a company by subscribing for shares when the company raises capital. Since Tuleva is already well capitalised, there’s been no need for that, and there doesn’t seem to be any in the near future either.

The second option is to buy shares from existing shareholders – and that’s exactly why we’re introducing this possibility by updating our articles of association. Two important amendments to the articles of association concerning membership capital were up for a vote at the general meeting.

Amendment 1: the option to transfer membership, along with the associated membership capital, to one’s heir.

A member of the Association may transfer their membership to another person, particularly if the member intends to transfer their assets to a future heir. The transfer of membership shall be decided by the management board. The supervisory council may, by resolution, specify the grounds on which the management board may refuse or approve the transfer of membership.

The option to transfer membership has been requested by some older Tuleva members who are of retirement age and no longer plan to invest. They’d like to pass their share in Tuleva, along with the associated membership capital, to their adult children. Transferring membership ends the transferor’s membership.

However, the special rights of Tuleva’s 22 founding members, which have been included in the articles of association from the start, cannot be transferred. These rights include the founding members’ right to elect 50% of Tuleva’s supervisory council, amending the articles of association and Tuleva’s purpose, and, when deciding on the merger, division, or dissolution of Tuleva, at least 50% of the founding members must agree.

Amendment 1 involves supplementing Articles 7.1 and 7.7, and adding two new Articles – 7.3 and 11.9 – to the articles of association.

Amendment 2: the option to transfer membership capital and membership bonus to another member. This would allow members who want to increase their capital in Tuleva to buy it from those wishing to sell theirs.

A member may transfer all or part of their membership contributions to another member of the Association (without transferring membership) in accordance with the terms and conditions for membership capital established by the supervisory council and subject to approval by the management board. For the transfer of membership contributions, the transferor and transferee shall submit a joint written application to the Association’s management board. Upon transfer of a membership capital contribution, the management board shall transfer the transferor’s membership capital contribution (or its relevant portion) to the name of the transferee. No member may acquire membership contributions in an amount exceeding 10% of the total membership contributions.

This option has been requested by Tuleva members who want to acquire a share in Tuleva. It also helps those who want to withdraw the membership capital they’ve accumulated because they need the money for other things. Until now, this has only been possible by leaving the association. But that isn’t reasonable, since it would cut off the possibility of staying involved in Tuleva’s activities. When someone leaves the association, their accumulated membership capital is paid out at book value, but that probably doesn’t reflect the full value of the capital. After all, we don’t just collectively own nearly 7 million euros worth of financial assets (most of it in our own pension funds) – we also own a fast-growing company with 79,000 customers.

Tuleva’s membership capital isn’t a security that can be traded on a daily basis. The amendment to the articles of association simply creates a way for two members to agree between themselves whether, how much and at what price the membership capital will change hands. To make this easier, we’ll set up a “membership capital notice board” on Tuleva’s website, where you can post if you want to buy or sell. The association must be informed of any transactions involving membership capital so the transactions can be recorded in the register and to ensure that no one person owns more than 10% of Tuleva’s membership capital.

The transfer of membership or membership capital must also be approved by Tuleva’s management board. The board will check that the transferee is indeed a Tuleva member and that their share of the membership capital doesn’t exceed the 10% limit.

The general meeting approved the amendments to the articles of association, which means the association’s supervisory council now needs to update the terms and conditions of the membership capital, and the management board must develop the technical arrangements for recording transactions. We plan to do this as soon as possible.

Amendment 2 involves supplementing Articles 8.7, 9.5, 12.4.1 and 12.4.2, and adding a new Article – 8.10 – to the articles of association.

More technical amendments to the articles of association

Two additional, more technical amendments to the articles of association were also put to a vote at the general meeting.

Amendment 3: we replaced the words “pension bonus” with “membership bonus”, and “pension capital” with “membership capital” throughout the articles of association. These terms have become established in communication with members and are clearer and more accurate. This won’t change the substance of the concepts.

Amendment 4: we updated the procedure for conducting general meetings in the articles of association. We’re already allowing members to cast their vote in writing before the meeting, even though this isn’t explicitly regulated by the Commercial Associations Act. We’ve based this on guidance from the Ministry of Justice and Digital Affairs, but in theory, it still carries a risk of legal dispute. On our lawyers’ recommendation, we added the option of advance voting to our articles of association to make the procedure for conducting meetings clearer.

Amendment 4 involves adding a new Article – 11.4 – to the articles of association.

All of the above-mentioned amendments were approved by the members at the general meeting. As the next step, we are preparing updated membership capital terms and making the necessary developments on the Tuleva website. This work is already underway, and the solution will be ready to use in a couple of months.

You can find the updated articles of association here.

How do we use membership fees?

Membership fees are used to develop the Association and to represent the interests of members. The fees of our first members were used to raise the fund’s initial capital, introduce Tuleva to the general public, and make preparations to start the fund, including application for an activity license from the Financial Inspectorate. From this point forward, membership fees will be used for the following activities:

Membership community management and communication

Development of Tuleva’s web page, blog, and other informational channels

The creation of proposals and influence analysis to improve the Estonian pension system, in cooperation with the Ministry of Finance and other state organizations

Development of Tuleva’s IT systems

Preparation and analysis of voluntary savings products and Third Pillar options

Your joining fee helps to bring well thought ideas with big impact to decision-makers.

Every euro saved gives a Swede almost a third higher pension than the same amount saved by Estonians. Estonia needs a smarter and measurable pension strategy.

As the first and only association representing pension savers, Tuleva is a credible partner for Ministry of Finance and state legislative bodies. We participate in pension strategy discussions, where next to the officials only banks and insurance companies used to be represented.

We help to make better laws. The laws that protect the people. The laws that maximize our profits from our, not banks’ savings.

We have our first achievements. For example

On Tuleva’s initiative, people in Estonia saved only during last year 1.5 million euros, because the fund managers are no longer allowed to charge high fees for changing the pension fund.

We sent a petition to parliament, signed by 2300 people, that proposes to reform how people can use their II pillar savings.

We do not organise demonstrations or spread random complaints. We are direct, we analyse issues and offer constructive solutions.

Tuleva is a social company with a goal to earn profit for its members.

Tuleva’s main principle is that people themselves save money for their future, using contemporary technologies and bypassing unnecessary middlemen and costs as much as possible.

Every year, each member who has transferred their second or third pillar to Tuleva pension funds, earns a member bonus. Member bonus is very small at first, but it will grow together with member’s pension assets. Bonus is transferred to your personal capital account at Tuleva. This is your ownership stake in Tuleva capital and this stake can earn you additional profit.

When Tuleva grows, our funds under management grow and we add new products to our offering, then the association will earn profit. The profit is then divided among members, as set in our Articles of Association.

As always with profit from entrepreneurship – this depends how well our venture is doing. The founders are convinced, that the 125-euro joining fee pays for itself many times over. But we do not give promises.

How is member bonus calculated?

At the end of each year

We calculate how many pension fund units each member had on average during the year in euros

Multiply this by 0,05% and transfer the resulting amount to member’s capital account

Every 5 years, members annual meeting decides whether to pay our accumulated profit as a dividend or keep it invested.

Tuleva is for people who care.

Every member has a vote on annual general meeting and has a right to elect and be elected to Tuleva’s board of directors and other supervisory bodies. This is the official part and it is very important.

Every day we share our ideas and experience among Tuleva members in our Facebook group, e-mail, phone and working groups. Among our community, there are people who care about the society and have very different skills. Many are ready to take responsibility for ensuring us a better future.

Tuleva team listens very carefully to our members and uses their ideas for making Tuleva better. We are only starting and believe that the power of thousands of smart people can be used for increasing our common good.

How does the calculator work?

Tax benefit is simple: the government pays you back the income tax on your third pillar contributions. Tax benefit applies to contributions that do not exceed 15% of your gross income or 6000 euros, whichever is smaller.

Your maximum contribution amount to third pillar is thus 15% x gross annual income. If your annual income is over 3333 euros per month (gross), then you can contribute to third pillar 6000 euros.

Tax benefit equals 20% x your third pillar contributions.

NB! Your tax benefit cannot be bigger than the income tax you have paid during the year. Thus: if your gross income is less than 614 euros a month, then your maximum contribution is less than 15% of your income. More precisely – your maximum contribution per month is then: gross monthly income x 0.964 – 500.

With less than 519 euro monthly income you are not paying income tax most likely and hence you do not have any tax benefit in contributing to third pillar.

Check the e-tax board to see how much gross income you have received this year

In the menu on the left, select Registers and inquiries -> My income. You can see the gross income earned this year on the basis of the data that payers have submitted to the tax office to date. Check whether income tax has been withheld from the payment amount or not, according to the payer. To do this, click on the name of the person making the payment, and in the last column of the summary information, you will see information about the withheld income tax.

NB! It is possible that your employer(s) have not yet declared the salary data for the last month(s) of the year. You can check this by clicking on the name of each payer.

If you know that income is still coming to your account this year, add it yourself.

Please note that all income that reaches your account this year will be included in the calculation for this year (if the December salary is received in January, it will be included in the next year’s income calculation).

You can also add income that you plan to declare in the income tax return this year: rental income, interest paid by crowdfunding portals, income from the transfer of securities or other property.

Don’t worry if you don’t know the exact amount of your annual gross income today. Calculate the approximate amount and then find the optimal third pillar money placement with the calculator. If the actual annual income turns out to be higher than expected, your contribution will simply be slightly below the income tax allowance limit. Nothing terrible will happen even if you put a little more than the tax credit limit in the third pillar. The law does not prohibit it – if you exceed the limit, you simply cannot get the income tax back.