After Parliament lifted restrictions on the use of the second pillar, the assets you accumulated in the second and third pillars are really yours. You can use them as you wish; you can take them out all at once or pay yourself a pension supplement every month. You can also keep your assets growing in the fund. What should you know to make the best decision?

This blog post and guide are based on our live show with Kristi Saare, chairman of the Tuleva supervisory board, on 7 April 2021. Tuleva members Taavi Pertman and Kristjan Lepik helped us think about the choices for the show, and our office manager, Pirje Keeroja, gathered feedback and members’ questions. You can watch the show here (in estonian):

What options do you have?

If you are 60 years or older (60 is currently early retirement age), you can do the following with the pension pillars:

1. Continue to save: money will continue to grow in the pension fund.

No age obligates you to take out your pension pillars. Nor does receiving a state pension mean you have to use your second or third pillar. If you work, regardless of age, a part of your salary and social tax will continue to go to the second pillar, and you can still contribute up to 15% of your income to the third pillar and receive an income tax refund on it.

Pension fund units can be inherited. When you are no longer with us, your heirs will receive your pension fund units in their pension accounts, or they can withdraw them in cash (20% income tax will apply in the latter case). You don’t have to file applications for bequeathing your fund units.

2. One-time payout: you take out all the accumulated money at once.

When you reach early retirement age, you can take out all or part of the money accumulated in your second or third pillars at any time (1). To do this, you need to submit a one-time disbursement application through Pensionikeskus or your internet bank, and the money will be credited to your bank account as follows:

- from the second pillar by the 20th day of the following month;

- from the third pillar within four working days of the application.

Upon payment, Pensionikeskus withholds 10% income tax. The amount paid does not count towards your taxable income or affect the amount of your tax-free income.

IMPORTANT! Any withdrawal application will permanently terminate your second pillar contributions (both the 2% from your salary and the 4% that the state contributes from the social tax paid on your salary). You can continue making contributions to the third pillar even if you are already withdrawing money from the third pillar at the same time – you will still receive an income tax refund.

3. Funded pension: you can take out the accumulated money as a monthly pension supplement.

You can draw a monthly pension supplement from the second and third pillars by submitting a funded pension application at Pensionikeskus. Unlike your state pension, the funded pension will not be paid until the end of your life but, rather, until the agreed term. Should you die earlier, your heirs will receive the remaining amount. If you live longer, you will have to live on a state pension or other assets after the end of the funded pension.

The amount of the funded pension changes over time, according to changes in the unit price of your chosen pension fund. This means that your remaining assets in the second and third pillars will continue to earn income in the fund (or losses in the event of a market downturn). Funded pension payments are exempt from income tax if your funded pension agreement is long enough – for example, at least 18 years if you sign the agreement at age 65 (2).

This is how simple your options are (3).

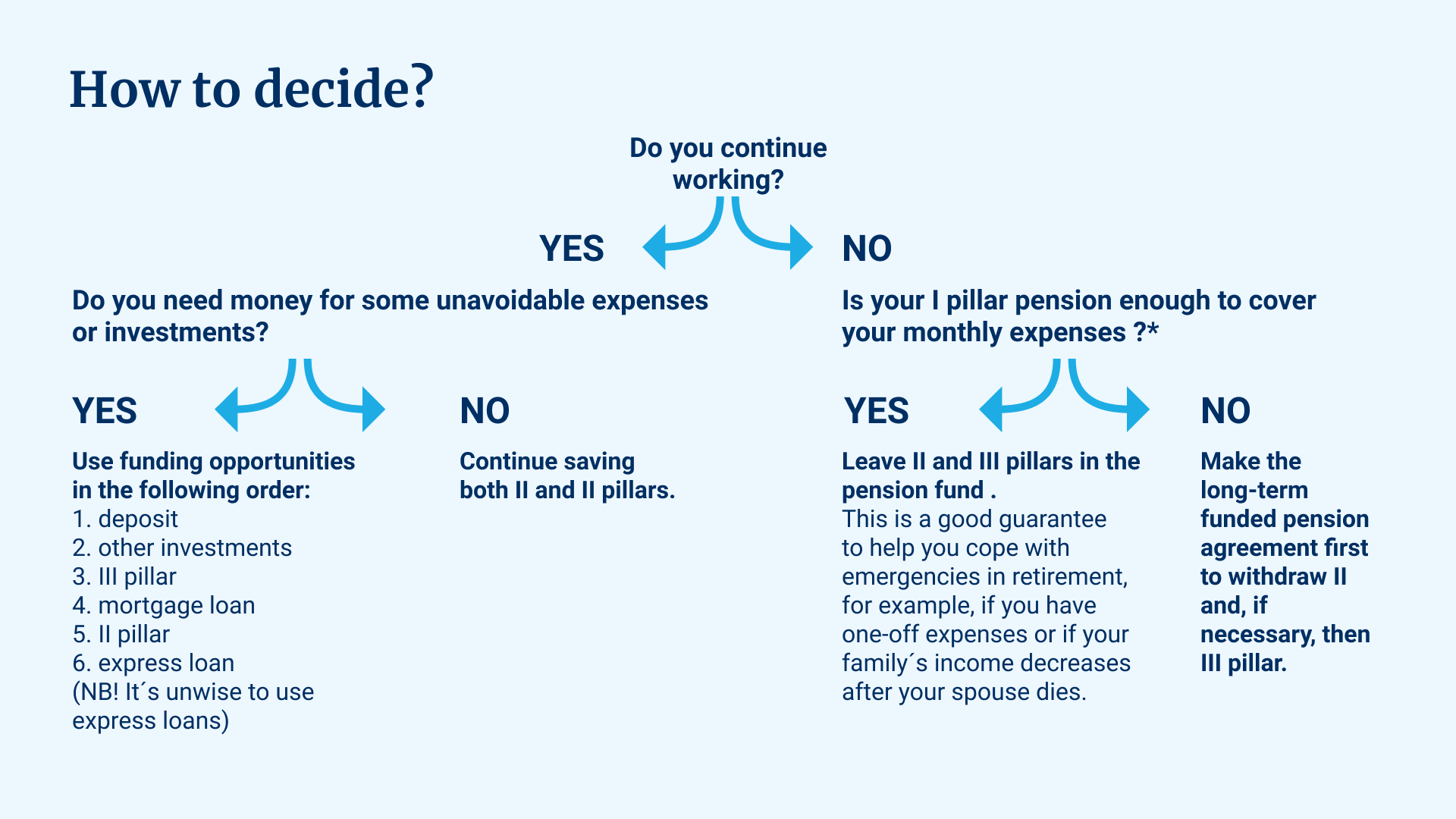

How should you decide?

In the past, the government’s idea was to very precisely prescribe how people should use the assets accumulated in the pension pillar. We believe that when a person has reached 60, they probably know better for what purpose they use their accumulated assets.

Here are a few questions that may help you decide.

Should you switch pension funds as you approach retirement age?

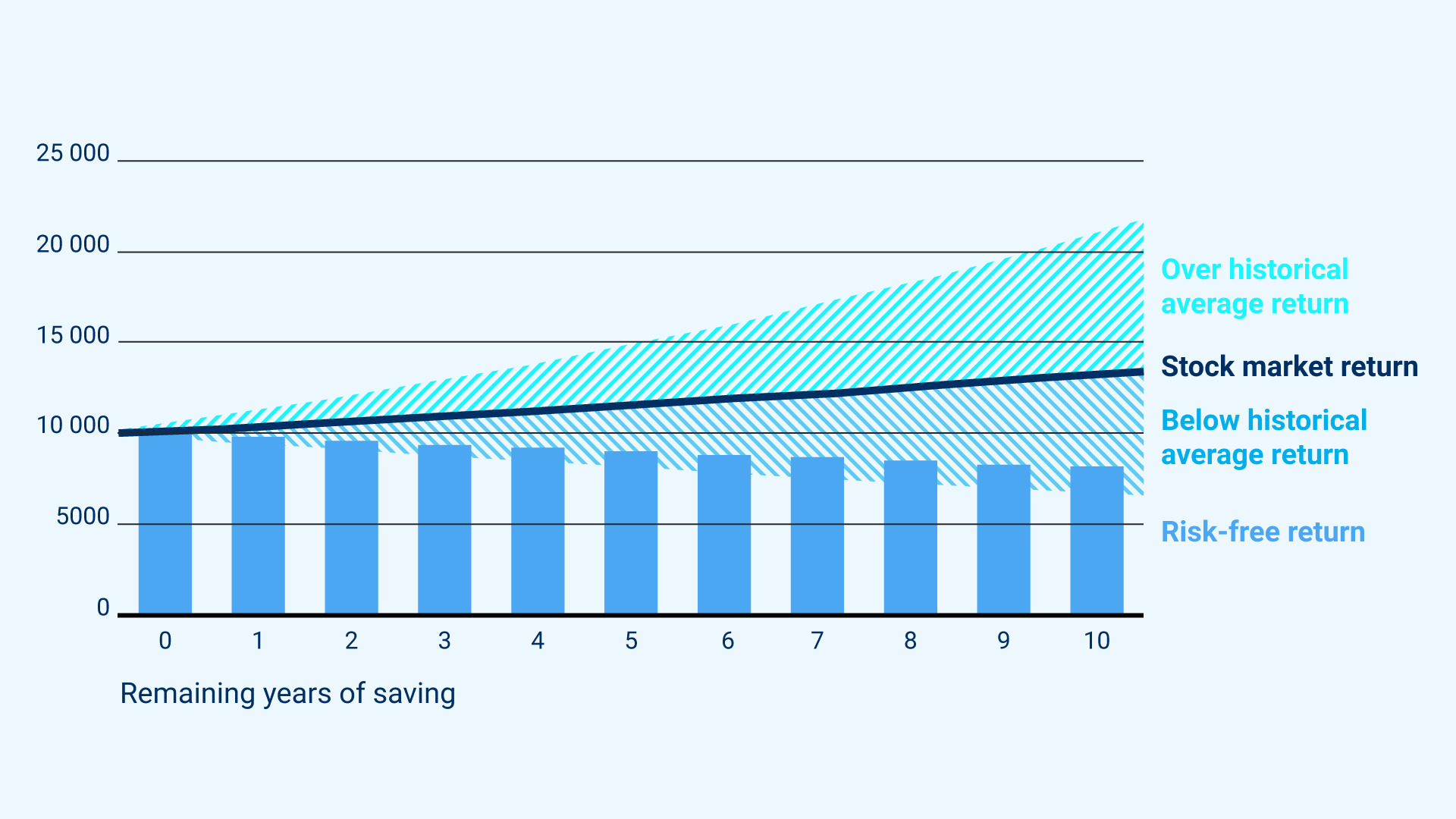

Management companies usually advise investors to move their assets to a conservative bond fund as retirement age approaches. Other pension funds invest a large part of their assets in stocks and generally offer much higher returns, but their unit price also fluctuates more. When markets fall, you will not have time to wait for market recovery before you retire.

When choosing a fund, always keep in mind that low-cost funds usually achieve better returns than high-cost funds.

Nobody likes it when the value of the assets they have accumulated over the years suddenly falls by 10, 20 or even 30%. Unfortunately, the risk-free rate of return today is 0%, and what’s worse, inflation reduces the purchasing power of a zero-return investment every year.

In conclusion, neither science nor the best experts can give a clear answer as to the right investment strategy or the most suitable pension fund for investors nearing retirement age. Then how can you decide?

- If you have reached your target amount and plan to withdraw money from the pension fund in a year or two to make your dream come true, then it’s perhaps better not to take any more risks. Fluctuations in the stock markets can thwart your plans. Move the accumulated second and third pillar assets to a bond fund, and you can be sure that when you withdraw the money after a few years, you will not be in for an awful surprise.

- If you don’t plan to withdraw all the money in the near future or instead want to leave it to your children, consider keeping the assets in stocks. This way, your children’s inheritance is more likely to grow larger over the decades.

- Most future retirees don’t yet know exactly when they will stop working or how much money they will need every month. Your working career can end for reasons beyond your control, for example, if your health fails or your employer decides to give up your services. Experts advise those approaching retirement age to keep at least one year’s expenses worth of assets in a rainy day fund – one where money can be withdrawn at any time and where its value does not fluctuate, i.e. a bank deposit or a conservative pension fund.

When choosing a fund, always keep in mind that low-cost funds usually achieve better returns than high-cost funds. Fees play an especially important role in the case of funds with a conservative strategy; in funds with higher fees, the value of your assets is quite certain to decrease in the coming years. Therefore, leave any fund that has fees higher than 0.5% per annum! You can find a comparison of fees here.

(1) As the pension reform was quite rushed, a few ways to use the money are still technically unavailable this year. In 2021, money can be withdrawn from the second pillar only in full and not in part. Also, it is impossible for technical reasons to withdraw third pillar money in 2021 through a funded pension. It will be possible in 2022.

(2) A sufficiently long term is one that is longer than your average life expectancy. According to Statistics Estonia, this means that if you are 65, your remaining life expectancy is still 18 years. In other words, if you at age 65 sign a funded pension agreement for at least 18 years, your income tax will be 0%, whereas, for a shorter agreement, it will be 10%.

(3) The law also allows you to take out a lifelong or fixed-term insurance contract for receiving your second or third pillar pension. Unfortunately, the fees of insurance contracts are currently so unreasonably high that insurance contracts are not even worth mentioning as an option. There is no reason to keep your pension assets at an annual cost rate of more than 1%.