Frequently asked questions

Why should I join the Tuleva Association?

By saving in Tuleva funds and becoming a member, you will get the most out of Tuleva. As a Tuleva member, you are not only a pension fund client but also a co-owner, and you can earn an owner’s income and decide on Tuleva’s development.

Tuleva’s idea is that people save money for their future together, leaving aside as many intermediaries and extra costs as possible – the more of us there are, the bigger the benefits from investing together.

How is Tuleva structured?

A commercial association is a business form like any other. The main difference between commercial associations and other forms of business is that in a commercial association every member has exactly one vote. In a public or private limited company the number of votes is dependent on the amount of shares you own

In a commercial association no one has the option to buy up other people’s votes or gain control of the association in any other manner. Profit sharing is carried out based on how much a member contributes into the association, not on how many shares she owns.

The founders of Tuleva believed that this form of entrepreneurship best represents a company that unites thousands of people. We don’t have distant investors, but we are all managing our money together and we all have the right to speak up about how our assets are managed, no matter how big one’s income or how much money one has managed to save yet.

The members of Tuleva Commercial Association are the owners. The members elect a supervisory board, which appoints the management board. Every Tuleva member has one vote at the association general meeting.

Tuleva pension funds are managed by Tuleva Funds, which is owned by Tuleva Commercial Association.

Is Tuleva a for-profit organisation? Who gets the profit?

Tuleva’s goal is to earn profit for its members.

If Tuleva earns a profit, then it will be divided between members based on the rules written in Tuleva’s Articles of Association – the way members have agreed to share the profit.

Firstly, each member will receive the membership bonus they have earned. The rest of the profit will be divided based on how much each member has contributed into the association’s capital.

Membership bonus is a bit like preferred stock dividend – it is paid to all members based on how much money they have transferred into Tuleva pension funds. A member’s capital share is dependent on how much money they contributed into the initial capital of the fund and how much membership bonus they have stacked up. The founders of Tuleva are subject to the same rules of profit sharing as all other Tuleva members.

What are the rights and obligations of Tuleva members?

Every member has the right to:

- Have access to important documentation pertaining to all activities of the association

- Participate in the general assembly and other Tuleva events

- Elect Tuleva management and apply for management positions

- Participate in Tuleva’s profit sharing based on predetermined rules

- Use Tuleva’s services and participate in members’ information sharing (for example via e-mail or in our closed Facebook group)

- Leave the association (after 5 years of membership have passed)

- Leave their assets as an inheritance to their designated heir

Every member has the obligation to:

- Comply with laws and follow the decisions made by Tuleva’s managerial board

- Pay a one-time membership fee

- Keep Tuleva’s business secrets

- Pay additional fees if decided so by the general assembly*

*This obligation has been included in our articles of association in the unlikely event that Tuleva has an unexpected need for additional capital. If a member refuses to pay additional fees which have been decided upon by the general assembly, they will lose their membership status.

Why is Tuleva Fondid AS a separate legal entity?

At this moment in time, Estonian laws do not allow commercial associations to manage investment funds (there is no real justification for this limit). Therefore we founded Tuleva Fondid AS, which is 100% owned by Tuleva Commercial Association. Based on Financial Inspection’s licence, Tuleva Fondid AS manages Tuleva World Stocks Pension Fund and Tuleva World Bonds Pension Fund.

What is the difference of being a client of Tuleva pension funds and being a member of Tuleva?

If you choose Tuleva’s pension funds you will become Tuleva’s client. If you also become a member of Tuleva, you will become a co-owner of Tuleva. Tuleva is a commercial association, which is owned by Tuleva members. We started Tuleva Fondid AS, which manages Tuleva pension funds. All Estonian people can become clients of Tuleva pension funds, you do not have to be a member to do so.

To become a client of Tuleva’s pension funds, you do not have to pay anything – you will instead instantly start to save money due to low management fees. It only takes 5 minutes to switch funds in your internet bank.

To become a member of Tuleva, you have to pay a one time membership fee (100 euros). Every member has paid a membership fee – this is every owner’s contribution to help develop our jointly owned association. The membership fee is one time only – there are no additional fees later on

Why do you want pension fund clients to also become Tuleva members?

The overarching idea of Tuleva is to bring people together to save money for their future, leaving out as many middlemen and unnecessary fees as possible. The more members there are, the cheaper it will be for us all to invest together using modern technological tools.

- By becoming a member you help fill our goals

Firstly, we plan to create voluntary savings products and other investment instruments to save money for the future.

Secondly, we will keep on fighting to make the Estonian pension system better for the people of Estonia, not just the banks or insurance companies. We will work together with the Ministry of Finance and citizen initiative project “Uue Eakuse Rahvakogu” helping to create better laws.

- Members earn a profit

Every year we calculate a membership bonus for all members who have transferred their second pillar funds to Tuleva pension funds. The bonus will be transferred to every member’s personal capital account at Tuleva. This will increase their share in Tuleva’s capital and this share will earn an additional return. If Tuleva gets bigger, and the funds start to manage more money and we create more investment products, the association will earn a profit, which will be divided up between members based on predetermined rules. As always, the size of the profit depends on how well we do as a business. The founders of Tuleva are more than convinced that the one time fee of 100 euros to join will be more than compensated in future returns, but we are of course not making any promises.

What is the membership bonus and how is it calculated?

Membership bonus is owner’s profit which is divided between each member who has transferred their second pillar assets into Tuleva pension funds. Membership bonus will be transferred to your capital account each year, which will increase your share in the association’s capital, which will earn additional profit. At the end of the year:

- We will calculate the value of units that a member had on average in Tuleva pension funds during the year

- Multiply that number by 0.05% and transfer the relevant amount to their membership bonus account

- Every 5 years we decide at our general meeting, whether to pay out the profits or keep the money invested

Can I become a member of Tuleva even if I haven´t joined the second pillar of the Estoninan system?

Yes, you can. We have members who support Tuleva’s goals and wished to help us reach them by paying the membership fee.

However, Tuleva was mainly established for people who are invested or plan to invest in second and third pillar pension funds and who plan to migrate their retirement plans over to Tuleva funds in future.

If you don’t plan to invest in the second or third pillar, or at least if you don’t plan to do so through Tuleva’s funds, Tuleva’s management can revoke your membership in the future as the organization is ultimately meant for people who want a mutual plan for growing their retirement nest egg.

Joining Tuleva is thus beneficial to you and generally a good idea only if you have invested or plan to invest in second and third pillar pension funds. But some of our members are just people who want to do their part to make Tuleva a success.

If I become a member of Tuleva, will my II pillar be automatically transferred to Tuleva pension fund?

No. If you haven’t changes your pension fund in your internet bank, you can do so immediately after joining Tuleva through our web app using your ID card or Mobile ID. Once you have made up your mind, it takes only 5 minutes of your time.

When I choose today Tuleva pension fund, can I later also join the association?

Yes. If you haven’t decided today if you want to become a member of Tuleva, then you can just transfer your pension to Tuleva pension fund. This doesn’t cost anything and takes less than 5 minutes in your internet bank. If you wish, you can become a member later. If not, there is no obligation. (The joining fee will increase in the future but we will let our pension fund clients know well in advance).

All Tuleva members must pay a one time fee of 125 eur to join. What is this money used for?

Membership fees are used to develop our association and to stand up for the rights of our members. From the fees paid by our first members, we made the necessary expenses to raise the fund’s initial capital, introduce Tuleva to the general public and prepare everything to get our pension fund started, including applying for an activity license from the Financial Inspection. From here on, membership fees will be used for the following activities:

- Membership community management and communication

- Development of Tuleva’s web page, blog and other information channels

- Preparation of ideas and influence analysis to improve the Estonian pension system in cooperation with the Ministry of Finance and other state organisations

- Development of Tuleva’s IT systems

- Preparation and analysis of voluntary savings products and better third pillar options.

I paid 125 euros, but it is not reflected on my membership capital statement. Why is that?

A joining fee and membership capital are two different things. The joining fee was a one-off fee that gave you a membership number, the right to have a say in Tuleva’s affairs, and the opportunity to earn a membership bonus.

The membership capital reflects your membership bonus, which is 0.05% per annum of the volume of your fund(s) held in Tuleva, i.e. your investment return. It will be transferred into your account each spring once the previous year’s annual report has been approved and the general meeting of the association has approved the decision.

What will happen to my money if I no longer wish to be a member?

If a member wishes to leave the association, then the membership bonus and capital will be paid out to them.

What will happen to my money if I pass away?

If a member passes away, the membership capital will be paid out to their heirs.

How does the calculator work?

The world's leading analysts have determined that fees are the surest predictor of returns: the lower the fees, the better prospects for growth. (And higher fees correlate with poorer results.)

Expected returns depend greatly on the evolving rate of return, and neither we nor anyone else are able to guarantee a 5% annual return.

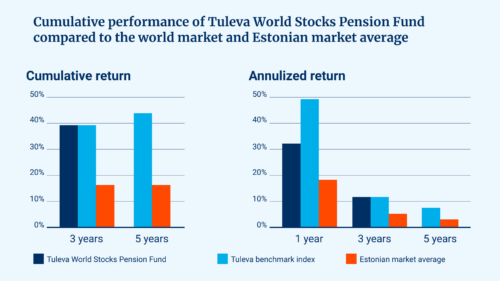

In a low-cost index fund your assets grow hand-in-hand with the average returns of world markets. Low-cost index funds have outperformed Estonian pension funds every year to date, but past performance is no guarantee of future performance.

Assumptions

Funds' average annual return before management fees

5%

Average annual salary growth

3%

Minimum eligible age

21yrs

Is our money in Tuleva as protected as in bank’s pension fund?

YES!

Financial Inspection

issued a licence to Tuleva fund manager and controls that our everyday operations comply with regulations.

Swedbank

is Tuleva pension funds’ depositary bank. Depositary bank approves every transaction with fund’s assets. Exactly like with bank’s own funds.

State guarantee fund

protects all pension fund investors against the worst in case fund manager causes harm to investors.