Tuleva’s mission is to help people accumulate capital efficiently and confidently. The first six months of this year tested the nerves of many investors: falling stock markets, rising inflation and war in Europe shook the sense of security.

While other pension funds shrank, we at Tuleva stayed firmly on course and continued to save. The volume of Tuleva pension funds increased during the six months despite the fall in the securities markets. In July, the total volume of our pension funds exceeded 400 million euros for the first time.

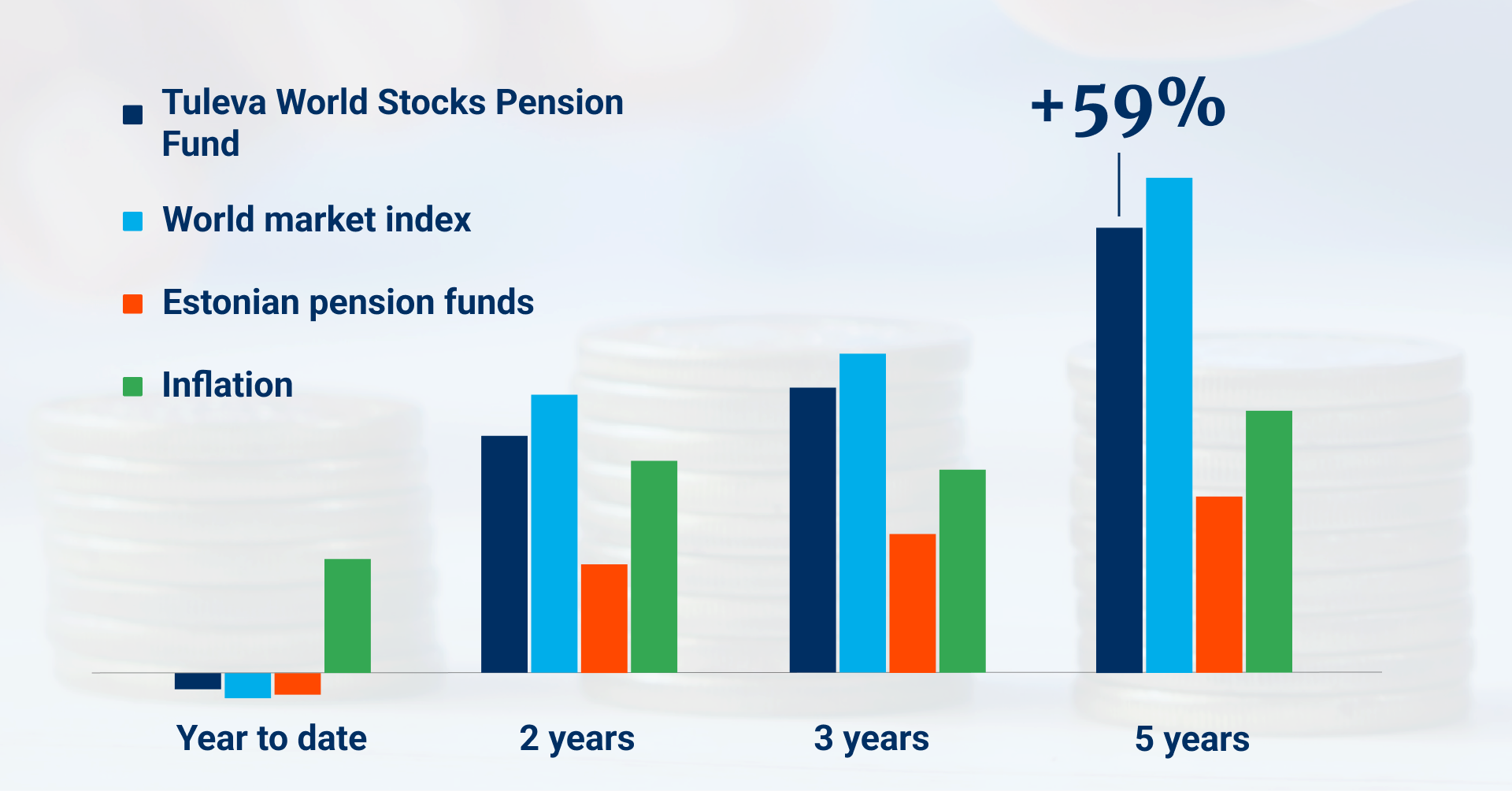

The performance of pension funds

In the first half of the year, world stock markets fell by 14%. Our pension funds imitate the world market both in ups and downs, and that is why the prices of our pension fund units also fell: both Tuleva World Stocks Pension Fund and Tuleva Third Pillar Pension Fund fell by 13%. Due to rising interest rates, world bond markets also fell, and together with them, the price of a unit in the Tuleva World Bonds Pension Fund fell by 11%.

Stock markets largely recovered before this report was finalised. Since early July, the world market index has risen by 13%, and therefore the unit prices of our equity funds have returned close to the level at the beginning of the year.

In five years, the price of a unit of the Tuleva World Stocks Pension Fund has increased by an average of 10% per annum. Tuleva Third Pillar Pension Fund will only complete its third year in October: since its establishment in October 2019, the price of its unit has risen by an average of 11% per annum. The price of the Tuleva World Bonds Pension Fund has fallen by an average of 0.6% per annum over the past five years.

This year, we also added inflation to the comparison, which has increased consumer prices by nearly 15% since the beginning of the year (from January to July), according to Statistics Estonia (annual inflation exceeded 20% at the end of July). In the past five years, inflation has reduced the value of money by an average of nearly 6% per annum. By the way, Tuleva investors can compare the performance of their pension account with both the world market average and inflation – log in and click on “World market return” in the “Your personal rate of return” drop-down menu and select “Inflation”.

How should you invest in a volatile world?

In good times and bad, it’s important to remember that there is no such thing as a risk-free return. Return is the reward that investors receive for taking on risk. Even a seemingly safe bank deposit that pays one or two per cent interest per annum does not guarantee that inflation will not render the return on your assets negative. Rather, the value of money in a bank deposit will quite certainly fall in the long run.

That is why at Tuleva we have chosen essentially the only way to save money, which ensures that the value of our assets will grow in the long run, hand in hand with the growth of the world economy. How do we do it? We consistently take a piece of our salary every month and use it to buy more shares in the world’s big companies. We confidently stay the course through good times and bad.

This does not mean that the market value of our assets will always go up. When the world economy is in recession and stock prices fall, the market value of companies and, with it, the value of owners’ assets, including ours, decline. It’s not pleasant, but you have to remember that there is also a good side to falling share prices – we can buy shares cheaper using new contributions. As the economy grows and prices rise again, our assets will rise too.

In the history of securities markets, stocks have always brought good returns to those investors who haven’t panicked, stopped saving or sold their investments in bad times. It’s easy to follow this principle with a pension pillar, as regular contributions to the second pillar (and for many investors, also to the third) are made automatically. You only have to make sure that your pension pillars grow in a low-cost index fund.

Tuleva investors continue on course

Most of the investors at Tuleva do this. In the first half of the year, 3,380 new investors joined Tuleva, which is a few per cent more than during the same time last year. More than 61 thousand people are now saving money in Tuleva pension funds. More and more people are contributing to our third pillar fund. In the first half of the year, more than 18 thousand people made contributions, totalling 15 million euros. This is 30% more than at the same time last year.

Therefore, the volume of our pension funds grew despite the market decline. The assets of other index funds following Tuleva’s example are also growing. On the other hand, the assets of the banks’ old funds have shrunk by more than 10%.

Is an index fund suitable at any time?

In short, yes. The history of the world’s investment funds shows that most actively managed funds underperform low-cost index funds, both in upswings and downswings.

Nevertheless, the financial sector is taking advantage of the turbulent times and people’s desire to find some security. High-cost actively managed funds are promoted as if they were somehow more “war-proof” or better protected against an economic downturn than index funds.

No Estonian fund manager has been able to beat the market average for a long period of time in the history of Estonian pension funds, and is not likely to do so in the future. The past half-year has not changed this pattern.

Since the beginning of this year, unit prices of supposedly actively managed bank funds have fallen pretty much in sync with index funds. Betterfinance has noted that most of our banks’ pension funds are likely to be “closet index funds”. Although such funds charge higher fees, they still passively follow a stock index under the guise of active management. In other words, the investor does not get any additional protection against market fluctuations for a higher fee.

LHV Pension Fund L stands out as an exception. However, it has another problem: most of the assets of this fund are not tradable on the stock exchange or are highly illiquid – their price in the fund’s report and in the calculation of the unit price might not reflect their actual current selling value (1). The LHV L unit seems to have lost less value in the market downturn, but we can’t be certain about that, as its assets may be overvalued (or undervalued).

When we talk about cars or wine, more expensive is often better, but in the world of investment funds it is very clear that higher fees mean lower returns. As data analysis consistently shows, funds that keep costs low and invest passively in the world’s largest companies are best positioned to achieve good long-term returns. That’s exactly what we do at Tuleva.

A step towards increased sustainability

In April, the Financial Supervision Authority approved the change to the terms and conditions of our pension funds, and we will start implementing the principles of sustainable investment from 1. of September. We have carefully prepared for this change for a long time.

Rather than creating an additional small “green fund”, we will make our large funds more sustainable. In exactly the same way as we don’t have a single good pension fund hidden among old, high-cost funds. Low fees and an awareness of the impact of our investments on the world are core values, which it would be cynical to apply selectively.

What will change in our funds from 1 September and what will remain the same?

We will reduce the carbon intensity of our investments by 15–20% and exclude approximately 200 companies from the portfolio that, according to experts, clearly don’t follow the principles of responsible governance.

The implementation of the sustainability principles does not lead to higher fees or change the expected return and risk profile of our portfolio. Tuleva’s passive investment strategy will remain in place. We will continue to consistently increase our participation in the global economy, as this has been proven to create the best conditions for achieving good returns in the long term.

All Tuleva investors know the carbon intensity of their investments, the most common measure of climate footprint. No other pension fund manager in Estonia has yet published this for all their funds. We hope that Tuleva’s example will help others make their activities more transparent, as has happened with fees. Measurement is important so that people can make a choice based on objective data, not green slogans.

We make changes to the portfolio so that it does not increase the fund’s costs. Read more and watch the discussion between Tõnu and Tuleva member Sten-Andreas Ehrlich on what we are changing and why.

Better laws

This half-year, our investors received excellent news: the government plans to allow contributions to the second pillar to increase from 2025. The draft law has been sent to the government. There are many of us who have taken full advantage of the tax benefit of the second and third pillars. We are waiting for the opportunity to accumulate even more capital by setting money aside regularly, automatically and tax-efficiently. This is exactly what larger second pillar contributions mean.

Plans for the future

We have set the goal for the next five years to help 100,000 Estonians regularly set aside at least 15% of their income for a better future. If we succeed, the assets of our mutual funds will increase to 2.5 billion euros. The larger the number of people that invest with Tuleva, the better the saving conditions will be for all of us.

We know that having good funds is not enough for people to start saving. We still have a lot of work to do to get people who have already opened an account in Tuleva to start saving properly (like Laura does: make sure that your second pillar accumulates in a low-cost index fund, and regularly set aside at least 10% or more of your income in the third pillar). For those who have already made the most of the pension pillars or want to save for their children, an additional savings fund will have to be added to our product range.

Even more people have not even heard of Tuleva. We have to reach those people who happen to have no higher education in finance or whose spouse or friend has not thoroughly investigated saving in pension funds.

The government’s support is also needed to improve laws and the national components of the system to remove many of the important barriers to saving. As the only organisation representing pension investors in Estonia, Tuleva is a partner for the state in the development of a smarter pension strategy. We do not limit ourselves to criticism, but offer systemically effective solutions. We will continue to help remove legislative obstacles so that every euro set aside will bring more benefits to the people of Estonia in the future.

We continue to look for ways to further increase the value of Tuleva for our members. Tuleva members decided to make better pension funds for themselves. With this, they started a revolution that has already and will continue to benefit all Estonian people. At the same time, the members of Tuleva started a rapidly growing enterprise, the value of which is growing alongside the assets of our mutual funds. Why can’t we float a minority stake in our fund manager in a few years?

We are a small team and we have to prioritise very decisively when choosing what we do. During this half-year, we will focus on two things:

- The government is working on an analysis of the sustainability of the pension system, the recommendations of which should be ready in the autumn. We keep our finger on the pulse so that the real concerns of pension investors are reflected in the analysis and the resulting recommendations, as well as the election programmes of political parties.

- Our business plan and terms of membership capital need to be supplemented. We will map the alternatives and involve experts from among our members to reach a suitable structure that supports the achievement of our goals, taking into account the values and special characteristics of Tuleva.

We wish you peaceful saving!

Tõnu Pekk

Tuleva management board member

Tuleva financial reports for first half of a 2022 are here (in Estonian).

(1) LHV Pension Fund L 2021 Annual Report, pp. 22–23.