Starting February 27, fees for all Tuleva funds have dropped to 0.28%. We lower our fees as soon as possible — whenever we can cover the costs of fund management at a lower rate. This time, the reduction was made possible by switching our depositary bank, which allowed us to lower our expenses.

Investing is a volume-based business. We can usually lower our fees when our assets under management have grown enough to spread costs across a larger pool of capital

The more of us there are saving together in Tuleva, the lower the cost per investor. This is the core of the Tuleva model.

Why are we lowering fees right now?

In addition to the growth in assets, this fee reduction is driven by a change in our pension funds’ depositary bank, which helped us cut costs. (1) A depositary is a bank that holds the fund’s securities and settles transactions. This ensures that our investors’ assets are always kept safe and separate from the fund manager’s own assets.

While Swedbank previously held our pension funds’ assets, SEB will be doing so moving forth. Since the depositary switch was already on the horizon at the beginning of the year, we launched our new Tuleva Additional Investment Fund (Täiendav Kogumisfond) directly with SEB.

As the depositary fee is one of our main variable costs, reducing it directly lowers the total cost of the funds. In Tuleva’s model, lower costs mean lower fees for all our savers.

Notably, our depositary fees were already among the lowest compared to other fund managers. Paradoxically, depositary fees are nearly twice as expensive in cases where the depositary bank belongs to the same group as the fund manager.

The graph shows Estonian pension fund managers’ depositary banks and their fees. We aren’t saying that fees paid within a banking group are inherently “unfair”, but it is a fact that intra-group depositary fees are higher. Data: 2024 Annual Reports of fund managers.

In connection with the depositary change, we also updated our pension funds’ key documents (terms and conditions, prospectuses, and key information). This does not change anything within the funds’ investment portfolios.

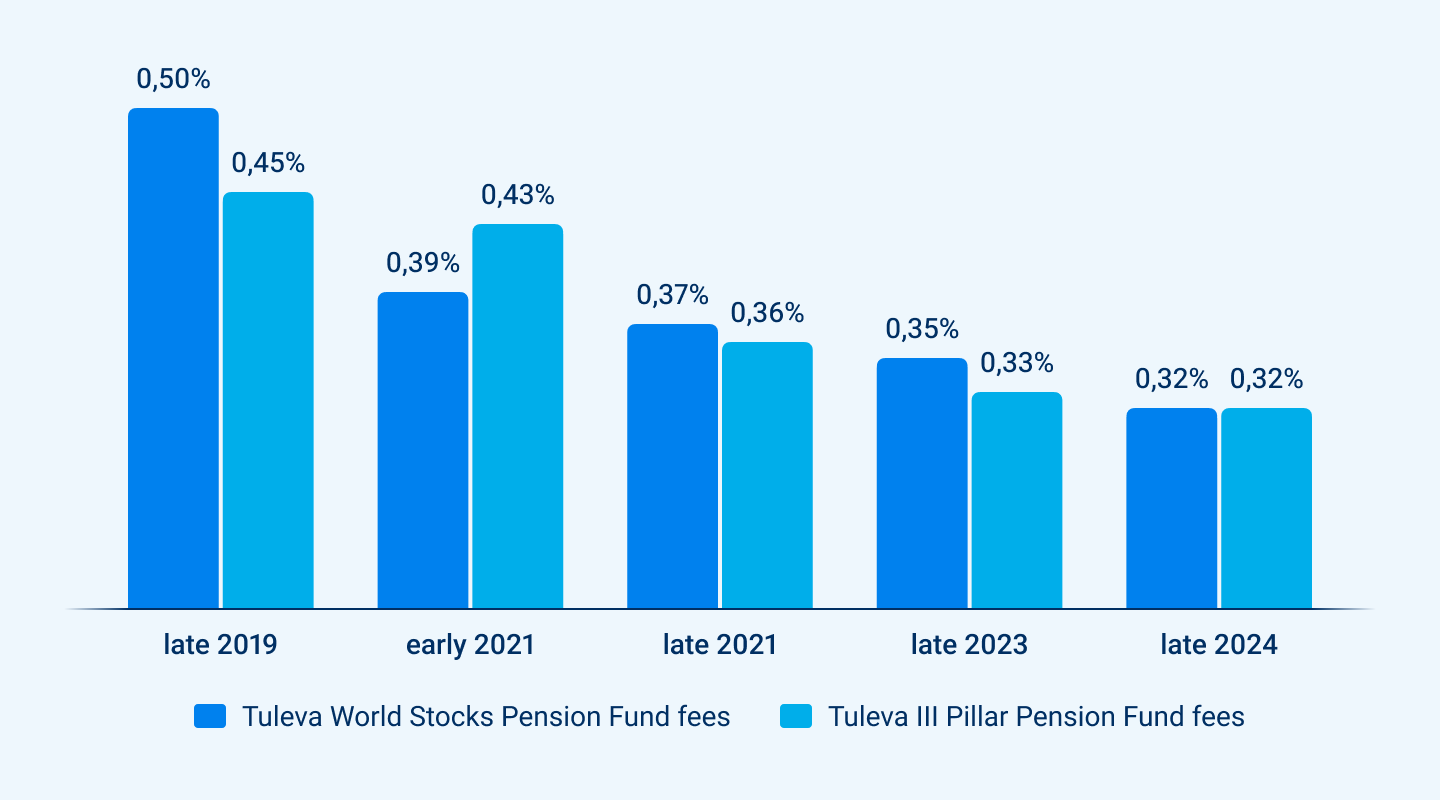

Tuleva fees are consistently falling

We aren’t pressured to lower fees by the state or by competitors. Tuleva’s owners are the same people who grow their wealth in our funds. We all have a direct interest in keeping costs under control. Furthermore, all our savers pay the same fee equally. We don’t offer a low fee in one fund at the expense of customers paying more in another.

The graph shows the fees of Tuleva’s two largest funds over the past six years. Since the end of 2024, the fees for all our funds have been identical, which also applies to our new Additional Investment Fund.

Unfortunately, data shows that Estonian pension fund fees, in general, are slow to decline. Because Tuleva is not a typical company, we can take a different stance: every time our costs decrease or efficiency grows, we pass that benefit on through lower fees.

Lowering fees is not a planned marketing campaign for us; it is the natural result of our business model. The more efficient our cost structure becomes and the more our assets grow, the more confidently we can continue lowering fees in the future.

The lower the fees, the more remains for the saver

A simple rule applies to investment funds: the less you pay in fees, the more of the returns earned by the assets stays with you. (2) Therefore, lowering fees is essentially the only thing that is guaranteed to improve your wealth’s performance.

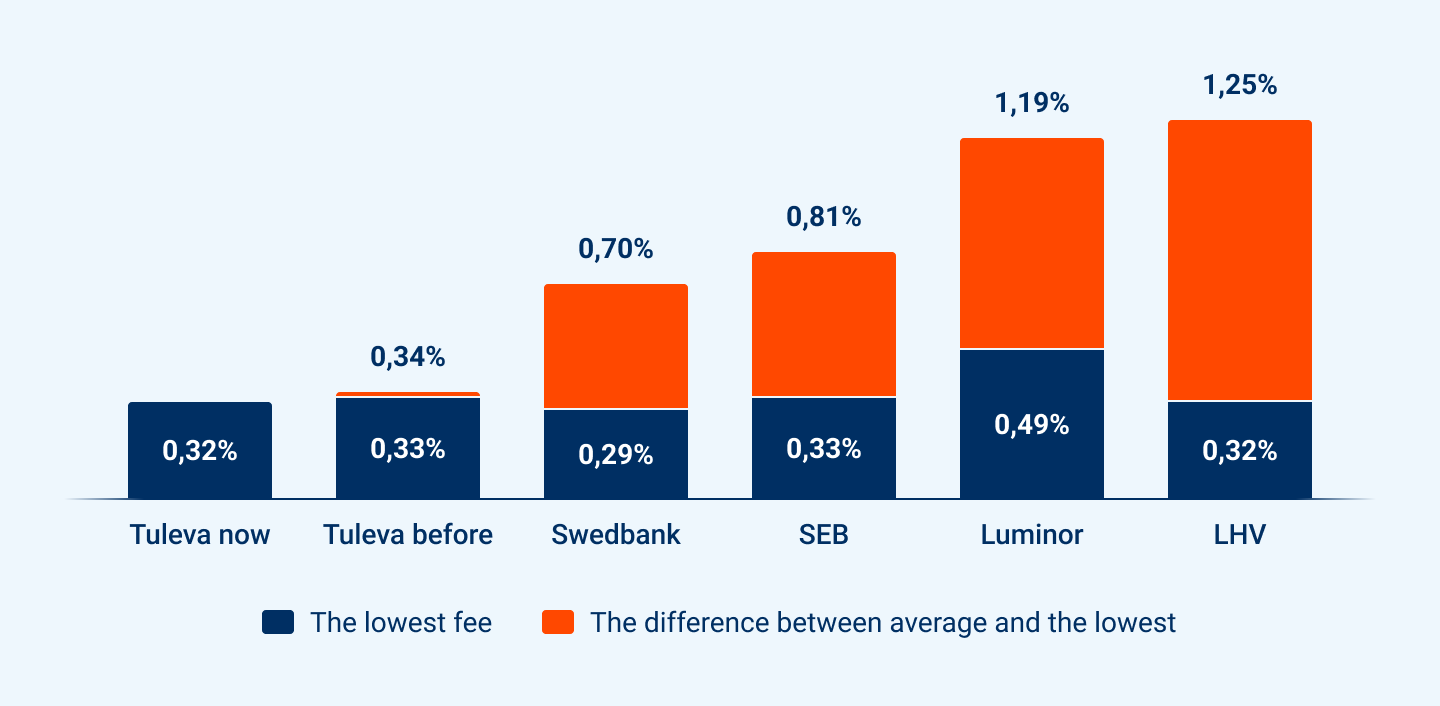

Pension fund fees may seem like small percentages, but their impact is long-term. As investors, it is vital to track the ongoing charges of a fund, which reflects the total cost. For example, for every €10,000 saved, you will now pay €28 per year in Tuleva funds, compared to €47 to €157 in some of the banks’ actively managed or life-cycle funds. (3) Over decades, these tens of euros in annual difference translate into tens of thousands of euros in your pension account.

See and compare how much you are paying in fees on your pension assets.

We previously managed to lower depositary costs and fund fees in autumn 2023. The depositary fee is just one part of our variable costs; we keep a “hawk eye” on all other expenses and constantly look for ways to reduce them whenever reasonable.

Income tax return: invest your tax refund in pillar III

Why is it wise to reinvest your income tax refund in your future right away? Because it’s just such a great way to take that first step without having to give up any of your regular income.

Opening pillar III takes a few minutes and costs nothing. Thanks to the tax advantage, pillar III isn’t just a great tool for saving for retirement, but also for achieving your other long-term goals. For every 1,000 euros you invest in pillar III today, the state will refund 220 euros in income tax. Make your first investment as soon as you receive your income tax refund. Once you’ve taken that motivating first step, set up a monthly standing order on Tuleva’s website to keep growing your portfolio with determination.

All of us saving in pillar III with Tuleva will, together, will receive nearly 15 million euros back from the state in 2024!

Already saving in pillar III?

Don’t forget to submit your income tax return. You’ll see the contributions you made last year automatically in point 9.2. You can transfer your income tax refund to pillar III right away, so it can start growing.

Note that if you made a contribution in the last few days of the year, it’ll probably not appear on your pre-filled income tax return and you should add the contribution amount to your return manually.

In this case, make sure the same contribution isn’t duplicated in next year’s income tax return. If necessary, you’ll need to reduce the pre-filled contribution amount accordingly. The Tax and Customs Board may also request proof of the payment date – for this you can submit, for example, the payment order or a bank statement. You can view the amount of your contributions made in 2023 by logging in to your pension account on Tuleva’s website:

Sometimes, you might wonder why your income tax refund amount differs from what you calculated based on your pillar III contributions and expected to receive. Keep in mind that the refund amount – or the amount of any additional tax due – is calculated based on all declared sources of income and tax credits combined. This means that your income tax refund amount is also influenced by factors such as how much of your tax-exempt income limit you’ve used, tax deductions for training expenses or home loan interest, additional tax obligations related to investments, and more.

The easiest way to check your income tax refund amount is to open the detailed calculation of your tax return, where you can see, line by line, which tax credits have been applied and in what amounts, as well as where additional tax obligations have arisen. For more detailed information on the calculation of income tax and declaring your income, contact the Tax and Customs Board directly.

The more investors we have at Tuleva, the less we all pay in fees. This is the essence of Tuleva’s model. Our assets under management have now surpassed the one billion euro mark, enabling us to lower fund fees once again. Starting November 14, fees across all Tuleva funds will be reduced to 0.32%.

Over the past year, Tuleva has experienced remarkable growth. Our funds now manage over one billion euros – nearly 70% more than a year ago. This growth is due in part to strong financial markets and a notable rise in stock prices. At the same time, investors have contributed an additional 192 million euros to our funds in the past year.

We lower fees as soon as possible

Investing is a volume-based business, and as the assets under our management grow, the costs per investor decrease. Every new euro added to Tuleva funds helps reduce fees for everyone.

Many Tuleva investors have already increased their contributions to the second pillar, giving us hope for continued growth in the future. This enables us to lower fees while maintaining a sufficient buffer to pay member bonuses and weather potential market downturns. Starting November 14, we are reducing fees across all Tuleva funds to 0.32%.

The chart below illustrates the downward trend in fees for Tuleva’s two largest funds. (1)

Tuleva members benefit further because we return a portion of our fees to ourselves. Each year, every member receives a 0.05% rebate of the value of their savings in Tuleva’s second and third pillar funds.

The more people save together with us, the more confidently fees will drop for all Estonian people

Lowering fees has a small impact on the average Tuleva saver, as fees decrease by only a few percentage points. It’s about the principle. Tuleva was created to increase competition among pension funds. We lower fees almost every year to make saving for retirement more affordable for everyone.

Lowering our fees does not make any single Tuleva fund the cheapest on the market. However, we are confident that all of our funds are good funds, as Tuleva remains the fund manager with the lowest average fees in Estonia by a significant margin. (2)

In the Tuleva model, everyone covers their own costs – no one else pays for your savings, and you don’t pay for someone else’s. In contrast, banks offer both low-fee funds and very high-fee funds, with the latter subsidizing the low-cost options.

The chart below shows the asset-weighted average ongoing fees of II pillar pension funds at pension fund managers as of 8th Nov 2024.

The less you pay in fees, the more you keep yourself

While pension fund fees may seem negligible, their impact over the long term is significant. Tuleva investors understand that saving on fees means having more wealth in the future.

One in five people who recently transferred their second pillar savings to Tuleva previously saved in the LHV L Fund. On average, those transferring from this fund had accumulated €14,500 in their second pillar. In 2024, they would pay a fee of 1.25%, amounting to €182. By moving their pension savings to Tuleva, they would instead pay just €46 – four times less. It’s human nature to postpone important decisions, but when it comes to pension savings, waiting truly costs money.

This is not some distant future projection or theoretical figure; it’s real savings. It’s like switching your family’s expensive mobile plans to more affordable ones – a small effort that saves money and generates returns for decades. You can calculate the impact of fees on your savings using our pension calculator.

Tuleva lowers fees because we can

We are not pressured by the government or competitors to lower fees. The owners of Tuleva are the same people growing their wealth in our funds, and it is in their interest to keep costs under control. Thanks to this, other Tuleva investors can also rest assured that saving with Tuleva will become even more affordable in the future. As more people save in our funds, we can continue lowering fees. The larger our fund size, the lower the costs for everyone.

Initially, Tuleva’s goal was to bring low-cost index funds to Estonia. Now we know that our greatest contribution is helping more people save wisely and consistently. That’s why we aim to cut through the noise and misleading advertisements to help people make informed decisions.

Moreover, the larger we grow, the stronger our voice in advocating for investors. Every euro saved strengthens our ability to push for a fair and modern pension system in Estonia.

See how much you’re paying in fees on your pension savings.

The fees for the Tuleva World Stocks Pension Fund will decrease from 0.35% to 0.32%, the fees for the Tuleva World Bonds Pension Fund will decrease from 0.38% to 0.32%, and the fees for the Tuleva Third Pillar Pension Fund will decrease from 0.33% to 0.32%.

Pillar III has gained significant popularity – it’s become the most common financial asset among people in Estonia. (1) Still, only around 20% of them use pillar III as a state-supported, tax-advantaged way to save. Many investors are put off by confusing information. There are several common myths about saving that need to be dispelled.

1. Retirement’s a long way off, and the money’s locked up in pillar III until you’re old.

Wrong – pillar III is flexible, and you can use the money you’ve saved at any time. Don’t let the word “pension” in the name mislead you. It’s worth reframing your view of pillar III: it’s an investment with good liquidity, as you can get the money from the pillar into your bank account in just a few days if needed.

You can continue saving again at any time in pillar III, regardless of intermediate withdrawals – unlike pillar II, where you have to wait 10 years after taking money out before you can start saving again.

2. It’s not really a tax advantage if I have to pay back income tax to the state when I take the money out, is it?

Well, yes and no. If you take the money out at retirement age, you can opt for regular payments, which are completely tax-free. If you wait until your 60th birthday to use the money you’ve saved (2), a reduced income tax rate of 10% will apply when you withdraw it.

If you really need to use the money earlier, you’ll have to pay income tax on the withdrawal. But that doesn’t take away the leverage your portfolio growth got from the state’s 22% “loan” in the meantime. (3) A simplified example: if you transfer 1,250 euros to pillar III and the state returns 250 euros to you as an income tax refund, your own contribution is 1,000 euros, but your pillar III portfolio is already worth 1,250 euros.

But still, if you get an income tax refund on the contributions but have to pay it again on payouts, the tax advantage disappears altogether, doesn’t it? That’s true, but none of us can predict exactly when we’ll actually need the money we’ve saved. In any case, it’s better to have built up some capital ahead of time. Pillar III is still the only tax-advantaged investment option, and as long as you don’t withdraw any funds, the “leveraged” portion of your portfolio can also generate returns.

3. I don’t know anything about investing and it’s too complicated!

Investing doesn’t have to be as complicated as some banks or financial gurus often make it seem. Success comes from sticking to simple rules that everyone can stick to: save regularly, don’t overpay on fees, and stay the course through good times and bad.

And as John Bogle, the creator of index investing, put it: “Don’t look for the needle in the haystack. Just buy the haystack.” The most convenient thing about saving in a pillar III index fund is that you don’t have to pick your investments yourself but can own small shares of thousands of listed companies around the world that operate in various sectors and regions, driving global economic growth. This way, you earn a slice of their profits without having to spend countless hours reading investment books and analysing companies.

4. The stock market’s hectic and who’s to say I won’t end up losing my pillar III investments altogether?

It depends – stock market fluctuations are inevitable. This is why it’s worth spreading your portfolio as widely as possible across different stocks (which is exactly what an index fund does) to avoid the excessive risk that comes with individual stocks. One of the rules of investing is that without risk, there is no return. Over the long term, it’s indeed been stocks that have delivered better returns than other asset classes.

By investing in the stocks of thousands of companies driving the whole market, i.e. in an index fund, you ensure that your assets are invested in the industries and countries that grow the fastest.

Regularly invest a small part of your income into a broadly diversified portfolio of companies around the world, so that at least part of your money is invested in the stocks of the next NVIDIA or a fast-growing economy.

5. Real estate and gold are tangible, after all, but the stock market is complicated, and who knows which stocks will actually perform better in the end.

Wrong – don’t forget that stocks have real value too. They’re ownership stakes in companies around the world, including their assets, and the profits they earn. Historically, equity stakes in the world’s leading companies have delivered returns that outpace inflation and go hand in hand with global economic growth. By saving in a broad-based index fund that invests in global stocks, you can be sure you’ve got shares in tech firms, real estate companies and gold miners.

If you started saving before 2021, you’ll be eligible for tax relief on your pillar III payouts as early as your 55th birthday.

From 2025, the income tax rate is 22%.

The second pillar is your asset: How to get the most benefit from It?

Kristi Saare and Tõnu Pekk have helped cut through the clutter of information about pension pillar reforms. Below you’ll find a summary that outlines how to withdraw from the second pillar and how to maximize its benefits.

The second pillar is truly your asset

While the second pillar was always legally your own, many didn’t feel it was theirs. Access to these assets was restricted, details on returns and fees were opaque, and there were no choices. Unsurprisingly, half of the Estonian population knew very little about their second pillar. However, those who continue to save in the second pillar until retirement age now stand to gain the most.

Thanks to recent pension reforms, the second pillar funds are undeniably yours. At any moment, you can submit an application to transfer the accumulated money to your bank account or direct it to your personal pension investment account, where you can buy stocks or funds by your choice. You can monitor on your pension account how much income this asset has generated for you and how much in fees is deducted from your investment each year. Essentially, the second pillar now operates just like any other financial account you might hold.

Gaining the most from the second pillar by continuing to save

The second pillar isn’t a ticket to paradise, but as Tuleva founder Jaak Roosaare puts it—it forms the foundation of a strong financial house. A great feature of the second pillar is that it’s already set up for you, continuously accumulating wealth every month without requiring any active effort on your part. Those who maintain their contributions until retirement age reap substantial benefits. Upon retiring, you’re no longer obliged to hand over the accumulated assets to an insurance company. Instead, you enjoy flexible access to your funds.

The law now allows individuals of pre-retirement age (currently 60 years old) towithdraw as much money as they need all at once. This can be particularly useful for significant expenses like insulating your home’s facade or covering essential medical costs. Withdrawals at this stage are subject to a reduced tax rate of 10%. Alternatively, you can opt for a fund pension, where payments are gradually disbursed to you while the remainder continues to earn returns in the pension fund. If this fund pension extends over a sufficiently long period, the tax on it can be zero. Ultimately, any money you don’t use in your lifetime will be passed on to your heirs.

The high cost of accessing second pillar capital prematurely

We’ve received numerous inquiries about whether it might be wise to withdraw from the second pillar to buy an apartment, forest land, renovate, settle debts, and so on. Before you make such a withdrawal to finance your dreams or business ideas, consider the cost. Generally, tapping into your second pillar funds before retirement age is an expensive decision.

For example, if you are currently 35 years old and earning the average salary in Estonia, you’ve likely accumulated just over 10,000 euros in your second pillar. Withdrawing these funds now would mean the state withholds 2,000 euros in taxes, and you would receive 8,000 euros. This might cover a thorough renovation of your kitchen or the purchase of a hectare of middle-aged forest land. However, if you delay this withdrawal, your second pillar funds could grow to about 35,000 euros in ten years. With this larger amount, you could undertake more extensive renovations or purchase more land—even if inflation increases prices in the interim. Conversely, the cost of that kitchen renovation or hectare of forest land would be substantially higher than it appears today.

What’s the rush? There’s no need to act immediately.

Remember, the chorus of intermediaries and advisors often urges you to ‘do something!’ However, when it comes to investments, sometimes the best action is inaction. Banks and financial institutions typically profit when you make moves with your money. The pension reform didn’t set any deadlines that require immediate action. You can withdraw assets or switch funds anytime.

(1) For this example, I am assuming that your salary grows by 3% per year and your pension fund’s return is 5% per year. If inflation is 2% per year, as it has been on average over the last 10 years, then 35,000 euros would be worth 28,700 euros in today’s money. If it’s 4% per year, then it would be 23,600 euros.

How do we use membership fees?

Membership fees are used to develop the Association and to represent the interests of members. The fees of our first members were used to raise the fund’s initial capital, introduce Tuleva to the general public, and make preparations to start the fund, including application for an activity license from the Financial Inspectorate. From this point forward, membership fees will be used for the following activities:

Membership community management and communication

Development of Tuleva’s web page, blog, and other informational channels

The creation of proposals and influence analysis to improve the Estonian pension system, in cooperation with the Ministry of Finance and other state organizations

Development of Tuleva’s IT systems

Preparation and analysis of voluntary savings products and Third Pillar options

Your joining fee helps to bring well thought ideas with big impact to decision-makers.

Every euro saved gives a Swede almost a third higher pension than the same amount saved by Estonians. Estonia needs a smarter and measurable pension strategy.

As the first and only association representing pension savers, Tuleva is a credible partner for Ministry of Finance and state legislative bodies. We participate in pension strategy discussions, where next to the officials only banks and insurance companies used to be represented.

We help to make better laws. The laws that protect the people. The laws that maximize our profits from our, not banks’ savings.

We have our first achievements. For example

On Tuleva’s initiative, people in Estonia saved only during last year 1.5 million euros, because the fund managers are no longer allowed to charge high fees for changing the pension fund.

We sent a petition to parliament, signed by 2300 people, that proposes to reform how people can use their II pillar savings.

We do not organise demonstrations or spread random complaints. We are direct, we analyse issues and offer constructive solutions.

Tuleva is a social company with a goal to earn profit for its members.

Tuleva’s main principle is that people themselves save money for their future, using contemporary technologies and bypassing unnecessary middlemen and costs as much as possible.

Every year, each member who has transferred their second or third pillar to Tuleva pension funds, earns a member bonus. Member bonus is very small at first, but it will grow together with member’s pension assets. Bonus is transferred to your personal capital account at Tuleva. This is your ownership stake in Tuleva capital and this stake can earn you additional profit.

When Tuleva grows, our funds under management grow and we add new products to our offering, then the association will earn profit. The profit is then divided among members, as set in our Articles of Association.

As always with profit from entrepreneurship – this depends how well our venture is doing. The founders are convinced, that the 125-euro joining fee pays for itself many times over. But we do not give promises.

How is member bonus calculated?

At the end of each year

We calculate how many pension fund units each member had on average during the year in euros

Multiply this by 0,05% and transfer the resulting amount to member’s capital account

Every 5 years, members annual meeting decides whether to pay our accumulated profit as a dividend or keep it invested.

Tuleva is for people who care.

Every member has a vote on annual general meeting and has a right to elect and be elected to Tuleva’s board of directors and other supervisory bodies. This is the official part and it is very important.

Every day we share our ideas and experience among Tuleva members in our Facebook group, e-mail, phone and working groups. Among our community, there are people who care about the society and have very different skills. Many are ready to take responsibility for ensuring us a better future.

Tuleva team listens very carefully to our members and uses their ideas for making Tuleva better. We are only starting and believe that the power of thousands of smart people can be used for increasing our common good.

How does the calculator work?

Tax benefit is simple: the government pays you back the income tax on your third pillar contributions. Tax benefit applies to contributions that do not exceed 15% of your gross income or 6000 euros, whichever is smaller.

Your maximum contribution amount to third pillar is thus 15% x gross annual income. If your annual income is over 3333 euros per month (gross), then you can contribute to third pillar 6000 euros.

Tax benefit equals 20% x your third pillar contributions.

NB! Your tax benefit cannot be bigger than the income tax you have paid during the year. Thus: if your gross income is less than 614 euros a month, then your maximum contribution is less than 15% of your income. More precisely – your maximum contribution per month is then: gross monthly income x 0.964 – 500.

With less than 519 euro monthly income you are not paying income tax most likely and hence you do not have any tax benefit in contributing to third pillar.

Check the e-tax board to see how much gross income you have received this year

In the menu on the left, select Registers and inquiries -> My income. You can see the gross income earned this year on the basis of the data that payers have submitted to the tax office to date. Check whether income tax has been withheld from the payment amount or not, according to the payer. To do this, click on the name of the person making the payment, and in the last column of the summary information, you will see information about the withheld income tax.

NB! It is possible that your employer(s) have not yet declared the salary data for the last month(s) of the year. You can check this by clicking on the name of each payer.

If you know that income is still coming to your account this year, add it yourself.

Please note that all income that reaches your account this year will be included in the calculation for this year (if the December salary is received in January, it will be included in the next year’s income calculation).

You can also add income that you plan to declare in the income tax return this year: rental income, interest paid by crowdfunding portals, income from the transfer of securities or other property.

Don’t worry if you don’t know the exact amount of your annual gross income today. Calculate the approximate amount and then find the optimal third pillar money placement with the calculator. If the actual annual income turns out to be higher than expected, your contribution will simply be slightly below the income tax allowance limit. Nothing terrible will happen even if you put a little more than the tax credit limit in the third pillar. The law does not prohibit it – if you exceed the limit, you simply cannot get the income tax back.