There’s no surer way to increase your future capital than by saving more yourself. Last year, we – Tuleva investors – set aside nearly 30% more money for the future than the year before. In five years, our annual contributions have grown from 35 million euros to nearly 170 million euros.

A rising savings rate combined with good returns is paying off: the assets of 7,400 investors at Tuleva have already crossed the €50,000 mark. Just five years ago, only a thousand of us had accumulated that much.

The chart shows the number of our investors over the years whose combined Pillar II and Pillar III assets in Tuleva exceeded the €25,000, €50,000, and €100,000 thresholds.

Becoming a determined investor with ease

In 2022, we set a goal to help 100,000 people save “determinedly”. We made a simple assumption: if a person regularly sets aside 15% of their income, they have a good chance of accumulating enough capital for the second half of their life. Over the last two years, we have taken a significant step towards this goal: as of this January, over 30,000 Tuleva investors are contributing to Pillar II at a higher rate.

The chart illustrates the distribution of our investors based on their Pillar II contribution rate and the size of their Pillar III contributions. We considered “determined investors” to be those with a Pillar II contribution rate of 4% or 6% who have also contributed over €1,200 to Pillar III over the last year. Those “on the path to determination” include: a) investors who have raised their Pillar II rate to 4% or 6% but do not actively save in Pillar III, and b) those who have not raised their Pillar II rate but actively save in Pillar III.

We know that the easiest way to save more and with greater determination is to do it automatically. That way, neither our own doubts (nor the providers of all kinds of spending opportunities) can derail our originally good plan. There is no simpler or more automatic savings system than Pillar II. That is why raising the Pillar II contribution rate is the most effective way to boost long-term savings: if you contribute 6% to Pillar II yourself, then together with the state’s contribution, your savings rate is already 10%! Add a little to Pillar III via a standing order, and you are firmly on the determined path.

What distinguishes us – Tuleva investors – from others is that we have made our decisions ourselves. No one has pushed us to switch our pension fund in a bank branch or a shopping mall. Therefore, it is no surprise that the savings rate of Tuleva investors is significantly higher than the market average.

The chart shows the share of investors who have raised their Pillar II contribution rate among our investors compared to the rest of the market. Source: Ministry of Finance (January 2026).

By the way, thanks to updates from Pensionikeskus, we can now see the Pillar II contribution rates of our Pillar III investors even if they use another fund for their Pillar II. This aligns with the behavior of Tuleva’s Pillar II investors: people who save with Tuleva are significantly more likely to have increased their contribution rate. This is good to know: our goal is, after all, to increase people’s savings rate regardless of where they save.

The chart shows contributions to Tuleva pension funds over the years. Source: Pensionikeskus.

A higher contribution rate, combined with wage growth and an increase in the number of investors, raised contributions to our Pillar II fund by 50%. One might have assumed that saving more in Pillar II would reduce Pillar III contributions. Recall the debates about whether it is more optimal to raise the Pillar II payment or fill up Pillar III first. However, it seems that most Tuleva investors have not let this theoretical debate distract them too much and have done the sensible thing.

First, raise the Pillar II contribution rate, because this must be done in advance: an application made before the end of November this year only takes effect in January of the next year.

Then, see if you can make Pillar III contributions, because you can make these for the whole current year – even on the last days of December.

For a vast number of us, larger Pillar II contributions did not prevent additional contributions to Pillar III. In a year, contributions to our Pillar III fund grew by 13%. The data shows that those who maximize their Pillar II contributions are more likely to make and increase Pillar III payments. In fact, those who raised their Pillar II contribution rate were more likely to continue or increase their Pillar III payments than those who did not.

For a great many people, the savings rate is surprisingly “stretchy” (or, in economic terms, inelastic relative to income). This is why activating investors continues to be such a rewarding endeavor: the effort made this year bears fruit for years to come. Of course, there are always people who simply don’t have enough money to save or who must temporarily reduce their savings rate because their income no longer covers expenses. Last year, nearly 1,000 of our Pillar II investors moved their contribution rate back to 2% (or reduced it from 6% to 4%). That is exactly the beauty of our pension system: you can adjust your strategy when circumstances change.

Employers are helping out

It is good to have helpers when trying to raise your savings rate. Some have a good friend or colleague to turn to, but the impact is greatest when saving is supported by your employer. Last year, several companies joined the ranks of Estonian employers who help their workforce save in Pillar III.

For example, Breakwater Technologies and Nabuminds recently decided, among others, to allow employees to simply tick a box indicating which portion of their salary they would like sent directly to their Pillar III account. In addition, they encourage saving by adding a little something of their own – 50 or 100 euros a month – to the accounts of those who contribute themselves.

It seems like a small detail, but the difference in savings rates is massive: while typically only one in five employees saves in Pillar III, the participation rate in these companies is 60% or more. It is also great news that state employees can now ask the State Shared Service Centre (Riigi Tugiteenuste Keskus) to direct a piece of their salary directly to their pension account. We even posted instructions for this on our Facebook page.

If your employer does not offer this option yet, but you believe your managers would be open to discussing it, let us know. I believe that the greatest opportunity for increasing the savings rate of Estonian people in the coming years lies right here in occupational pensions.

By the way, you don’t always need to create a new system or additional payroll costs in a company. In November, several progressive employers sent a letter to their teams about raising the Pillar II contribution rate. We did a small survey which revealed that if company managers really want employees to save, the results usually follow. There are companies where 80% of employees have raised their Pillar II rate or 95% save in Pillar III, and then there are “ordinary” companies.

The Additional Investment Fund is ready

When Kristi and I were recording the last episode of the Tuleva Podcast (in Estonian), she sighed: “Finally ready!”. We knew a long time ago that for many of us, pension funds alone are no longer enough—people want to save more. We promised to add another fund to our selection: one where you could contribute outside of the pension pillars, open an account for your child, or invest your personal company’s (OÜ) cash reserves.

In the meantime, the pension pillars improved: it became possible to direct 10% of income to Pillar II instead of 6%. This delayed the creation of our new fund, but we completed the work last year, and the new fund will start operating on February 2nd.

Creating the Additional Investment Fund (Täiendav Kogumisfond) gave us the chance to tackle tasks that had been waiting for a cleanup for a long time. At the beginning of the year, we did a “spring cleaning” of our internal rules, greatly aided by TGS law firm (along with Tuleva co-founder Kirsti Pent and Maria Suurna). After that, Maria actually came to work for us and has been responsible for compliance and risk control as a board member since the spring.

In the autumn, our office was full of developers because the platform for the new fund was built, once again, during Tuleva sprints. In the intervening years, we had allowed ourselves the luxury of hiring developers full-time. While development work was steady during that time, I always felt that in addition to one or two good IT experts, there are dozens of super-talented contributors among Tuleva members who would happily pitch in. That is why we went back to sprints.

Our assets grow together with our investors’ assets

Asset management is a volume business: the larger the volume of assets, the better the saving conditions become for everyone. While in Tuleva’s early days our growth was driven primarily by people switching funds, today the main growth engine is the monthly contributions of us, Tuleva investors. In five years, these have nearly quintupled. In our small market, it is more sustainable long-term to grow assets by having every person own more assets, rather than simply having more people.

The chart shows the sources of Tuleva’s asset volume growth by year. Asset volume growth is also influenced by the rise or fall of the global market – more on that below.

We have quietly grown into the second-largest fund manager by contributions. Last year, we surpassed SEB and LHV with our Pillar II Stocks Pension Fund. Our growth comes mainly from our investors increasing their contributions, not from aggressive marketing.

The volume of assets in our pension funds grew by just under 30% over the year, reaching nearly 1.4 billion euros. Thanks to this, we were able to lower fees again in November. The ongoing charges of our pension funds are now 0.29% per year.

Tuleva’s asset volume and the average ongoing charges of our funds, along with a forecast of how much our fund fees could drop further if asset volume continues to grow (grey bars).

How to win trust?

Unlike contributions, the number of people joining our Pillar II has remained at a fairly similar level over the years. Tuleva funds have never been at the top of the “fund switching leaderboards”. We don’t have the kind of tools that nudge huge numbers of people who aren’t making a truly conscious decision.

However, a window opens from time to time when people suddenly take an interest in Pillar II. The pension reform of 2019–2020 was one such moment where people looked for “beacons of truth” and often found them among our investors (from influencers to financially savvy colleagues or relatives). The major campaign in 2024 regarding the increase of Pillar II payments also brought us a multitude of new exchange applications. Increasing the contribution rate last year did not generate enough excitement to set Pillar II in motion.

It is hard to create such big changes ourselves, but we can ensure that we have enough of these good “beacons of truth” among our investors, to whom people look at critical moments. That is why we did a lot of work regarding the influencer regulation proposed by the Financial Supervision Authority. It seemed to us that it excessively restricted the ability of financially literate individuals to share their knowledge. We gathered the opinions of financial literacy promoters known to us to send a well-argued position to the state. We are waiting for the amended proposal at the beginning of this year.

The best way to grow assets through fund exchanges is still to ensure that people who have already started saving with us do not leave lightly or in disappointment.

The volume of assets leaving via Pillar II exchange transactions is shown as a percentage of the fund manager’s total asset volume. Sources: Pensionikeskus, Tuleva calculations.

Market growth and equities suit the long-term investors

A significant part of the growth for both Tuleva as a whole and for each of our personal pension accounts comes from returns. Over a long period, we expect returns to contribute at least as much as our own contributions. One could half-jokingly say that for most of us, income is not high enough to accumulate sufficient capital for the future without the help of returns.

The chart shows the returns of our Pillar II and III equity funds over the last 1, 2, 3, and 5 years compared to the global stock market index (MSCI ACWI), the average of Estonian Pillar II funds (EPI II), the average of Estonian Pillar III funds (EPI III), and Estonian inflation. Sources: Pensionikeskus 31.12.2025, MSCI, and Statistics Estonia. Past performance is not a guarantee of future results.

Our goal is to achieve a long-term result as close as possible to the global market average return. We know that for shorter or longer periods, returns can be near zero or largely negative. The past year also showed that significant mood swings can happen in the global market over a short time.The trade war unleashed by the USA at the beginning of the year took stock markets down 18% at one point. It didn’t matter whether the companies were headquartered in the USA or elsewhere. The global economy is tightly interconnected, and a change in one region often affects many.

Seeing a sudden drop of 10%, 15%, or even 30% in personal assets is unpleasant. Financial sector intermediaries therefore quickly offer tools to reduce volatility. Unfortunately, they all have one flaw: they all significantly reduce long-term returns. It is no wonder that the return of Estonian Pillar II investors has been poor for years: fund managers kept a large part of investors’ assets in low-yield bonds or even bank deposits to “avoid volatility”.

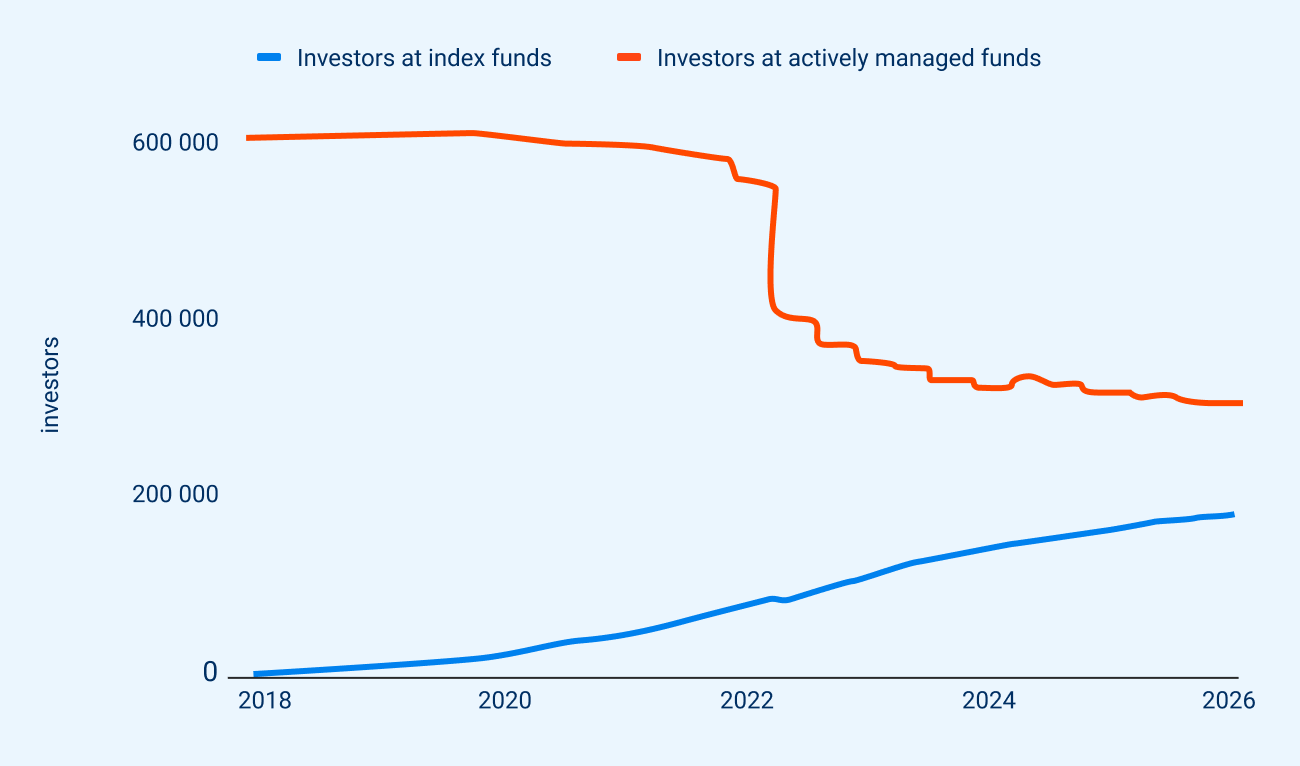

The situation has improved in recent years. While in the 2016–2020 period the global stock market grew by an average of 10% per year and Estonian Pillar II pension funds barely 3%, the ratio for the last five years was better. From 2021–2026, global stocks produced 12% and Estonian Pillar II pension funds 8% per year. Behind this are the investors themselves – increasingly, the assets of Estonian people are growing in index funds that invest 100% in equities.

The chart shows that more and more Pillar II investors are choosing a low-fee index fund instead of an actively managed fund. Source: Pensionikeskus, Indrek Seppo.

However, a large portion of Estonian people’s assets still does not earn a fair share of the return offered by the global market. We cannot blame only high fees here – they are just part of the story (though not an insignificant one). Fear and established habits also play a part. For example, the idea that “as retirement approaches, one should supposedly prefer bonds over stocks”. I do not agree with this.

The chart shows the returns of our Pillar II bond fund over the last 1, 2, 3, and 5 years compared to the global bond market index, the Estonian Pillar II conservative funds index (EPI10), and Estonian inflation. Sources: Pensionikeskus 31.12.2025, MSCI, and Statistics Estonia. Past performance is not a guarantee of future results.

Global bond markets have not offered acceptable long-term returns to investors. Although global central banks lowered short-term interest rates, long-term interest rates rose slightly. This lowered bond prices. The drop in the US dollar also had a negative effect on the return of the Tuleva World Bonds Pension Fund. Namely, the portfolio of this fund holds approximately 10% in US government bonds denominated in dollars. The fund’s unit price fell by 0.5% over the year. Over five years, the unit price has fallen by an average of 2.5% per year.

…

We don’t know any secret tricks to earn returns exceeding inflation in the long term without taking risks. Instead, we look for ways to better tolerate volatility. We know that the best protection against risk is time: the longer the period we look at stock returns, the smaller the fluctuations become. The good news is that we remain long-term investors even when we are over 60.

Upon reaching retirement age, it is most sensible to use your money in the pension fund via a drawdown contract (in Estonian: fondipension) – periodic withdrawals that allow you to redeem accumulated fund units tax-free, bit by bit, over a couple of decades. All this time, the unwithdrawn units continue to earn returns. This means that even a 60-year-old person has another twenty years to invest and earn returns.

Therefore, we changed our fund terms in the spring. Our equity funds are suitable for saving through life, regardless of age. A pension fund is a good tool for hedging equity risk: it is best to make both contributions and withdrawals gradually. By putting a piece of our salary aside every month, we buy stocks when they are expensive and when they are cheap, achieving an average over the long term.

Most of our investors over 60 already follow this recipe and save in equities anyway. Now, this is also clearly stated on our website and in fund documents.

The chart shows that more and more of our investors continue to save in the Pillar II equity fund even at age 60+.

Financial result: larger volume enables even lower fees

We lowered fees twice last year and still earned a decent profit. We collected a total management fee of 2.7 million euros. This is 22% more than the year before. The average volume of assets grew by 29% over the year.

Our gross margin, i.e., the part of revenue from which we can cover our fixed costs and profit, grew to 2.2 million euros (22% more than the year before). Our gross margin is best measured as a ratio to the volume of fund assets. Last year it was 0.19%, dropping by 2 basis points from the 0.21% level a year ago.

The chart shows the annual average volume of Tuleva funds, ongoing charges, management fee, and gross margin.

There are always two main sources for lowering our fees. If variable costs fall – for example, the depositary fee or guarantee fund fee – we immediately reduce fees by the same amount. Likewise, if we manage to negotiate lower fees for BlackRock funds, this also immediately reduces our ongoing charges. Additionally, volume growth allows us to cut the fee at the expense of our own margin. Thus, a falling gross margin is our goal: the larger the asset volume grows, the less we need to charge to cover costs and profit.

According to initial estimates (the audit is still ongoing), our fund manager earned an operating profit of 0.2 million euros for the year. A significant difference from previous years is that, starting from the past year, our fund manager pays a license fee to the association (Tuleva Tulundusühistu), which equals 0.05% of the average volume of our funds’ assets. Last year, we transferred nearly 0.6 million euros to the association’s account. Thus, on a comparable basis, we earned twice as much profit as the year before.

As always, the change in the value of pension fund units owned by us is added to (or subtracted from) our net profit. Last year, this added 0.6 million euros to the result (in 2024, it added 1.5 million euros).

2025

2024

Service fee income

2 687 909 €

2 191 358 €

Service fee expenses

−1 067 779 €

−365 291 €

Financial income and expenses

Interest income

15 213 €

11 457 €

Change in fair value of financial investments

608 753 €

1 521 513 €

Labor costs

−908 884 €

−962 955 €

Miscellaneous operating expenses

−485 397 €

−496 257 €

Other business income

67 120 €

82 931 €

Operating profit (EBITA)

229 934 €

407 869 €

Depreciation of fixed assets

−63 035 €

−41 917 €

Net profit/loss for the reporting period

853 899 €

1 940 838 €

Table: Key financial indicators of Tuleva Fondid AS. 2025 results are not yet audited.

The year ahead: new depositary, more automation

We are starting the new year with a significant change in our operations. We have used Swedbank as our depositary bank for eight years, and now we are changing providers: starting in March, our depositary bank will be SEB. The new fund will start with SEB immediately.

The list of depositary service providers in Estonia is restricted by law: one must hold an Estonian credit institution license. Therefore, the world’s largest depositary service providers cannot offer us services: no one will apply for a credit institution license here for such a small volume. So, in reality, we only have a choice between two providers, SEB and Swedbank. I believe we are paying the lowest fee in the market, but in international competition, there would still be room to cut costs further.

What will the new year bring for the funded pension system?

Our neighbor Lithuania started the new year by implementing its funded pension reform. Since the beginning of January, Lithuanians can withdraw the money they contributed to Pillar II, along with all earned returns. We are carefully watching these developments to better participate in the (re)starting pension reform debate here. (4)

In the funded pension reform debate that took place over five years ago now, I managed to get a word in for a moment during a stormy TV debate. “It’s good that we got Tuleva up and running so quickly. There are already enough of us to save money more effectively together. We are no longer affected by whatever decisions the government makes or fails to make,” I managed to add to the discussion before it went back into the twists and turns of comparing Pillar I and Pillar II.

Today, this is even more true than back then. Naturally, we take advantage of the tax deductions and opportunities created by the state’s funded pension system, but the state does not have to stand guard over the effectiveness of our investing. Nevertheless, we actively participate in the discussion. After all, we continue to be the only organization that truly represents the interests of the people whose money is accumulating in pension funds. (5)

(1) We based this on the estimate by the Arenguseire Keskus, stating that within the Estonian pension system, a person who regularly saves 15% of their salary secures a 70% replacement rate by their 65th birthday. This means that upon retiring, they can achieve an income equal to 70% of their last salary through the Pillar I (state pension) and accumulated capital. Since we do not know the income level of many of our investors, we use the Pillar II contribution rate as the simplest proxy for estimating the savings rate.

(2) The Financial Supervision Authority requires fund managers to clearly warn that the “state contribution” to Pillar II is not free but reduces the size of a person’s Pillar I. We are not big fans of such vague warnings (called disclaimers). Just as the “read the terms and consult an expert” warning means nothing in reality, knowing that the portion of social tax directed to Pillar II “might reduce” your Pillar I pension is of little help to a person. Therefore, instead of an empty warning, we created a simple tool (in Estonian) that calculates exactly how much less Pillar I pension units you have earned over the last 8 years due to participating in Pillar II, and what you have gained in return.

(3) In October of last year, the Financial Supervision Authority shared a draft document outlining good and bad practices for those sharing financial knowledge, which received quite a lot of public attention in the Estonian media.

(4) For this reason, I accepted the invitation from Tuleva co-founder Henrik Karmo to become a member of the supervisory board of the modern Lithuanian pension fund manager GoIndex UAB. I am also a member of the supervisory board of Wise Assets Europe AS, a subsidiary of Wise plc led by another Tuleva co-founder, Kristo Käärmann. The latter company offers Wise customers a possibility to hold their cash in their Wise accounts in either a money market or an equity fund.

(5) The TV show “Suud puhtaks” (in Estonian) on April 9, 2019. My turn to speak only came during the very final minutes.

Where does the Tuleva Additional Investment Fund invest?

The Tuleva Additional Investment Fund invests 100% of its assets in global stock markets, just like our Pillar II and III equity funds. When you invest in the Additional Investment Fund, you aren’t just buying fund units – you are gaining a stake in the world’s largest companies.

Which companies do you own through the fund?

The fund tracks the MSCI ACWI index, which includes nearly 2,500 of the world’s largest publicly traded companies from both developed and emerging markets. Chances are, you already use their services every day. (1)

For example, when you:

buy a phone (Apple, Samsung);

order a package online (Amazon);

install Windows on your computer (Microsoft);

search for something online (Google, Meta);

use a credit card (Visa, Mastercard);

drink a soda (Coca-Cola);

take medicine (Eli Lilly, Novo Nordisk, Astra Zeneca);

buy a new car (Toyota, Tesla, Mercedes, VW Group, etc.);

buy a household appliance (Samsung, LG, Whirlpool).

Among these 2,500 global giants, you’ll also find some of Estonia’s largest employers: by investing in the fund, you own a piece of Ericsson, Swedbank, and Wise.

Each company is represented in the portfolio according to its market value. If a company’s shares make up 1% of the total value of the global stock market, our fund also invests approximately 1% of its capital there. This means the top holdings change over time. For instance, in 1996, the heavyweights would have included General Electric, Coca-Cola, and Shell; in 2006, Exxon, Microsoft, and Citigroup; in 2018, Apple, Microsoft, Alphabet, and Alibaba; and today, Nvidia, Apple, Alphabet, and TSMC. (2)

Don’t look for the needle – buy the haystack

How did we choose these specific stocks for the fund? The answer is simple: we didn’t.

Our fund is passive, meaning we don’t try to outsmart the market by picking individual stocks. Most funds that attempt to do so end up with lower returns than the market average in the long run, even if they get lucky for a short period. Instead of trying to find the one “needle” in the haystack that will grow the most, we buy the entire haystack.

Technically, we achieve this by purchasing units from six major fund managers (Vanguard, BlackRock, Amundi, DWS (Xtrackers), Invesco, and BNP Paribas) to replicate the MSCI ACWI index at the lowest possible cost. (3)

In practice, this means we exclude about 200 companies from the nearly 2,500 in the MSCI ACWI index. The largest exclusions include Philip Morris (tobacco), Boeing (missiles in addition to aircraft), and Altria (tobacco).

Why so much exposure to the US and the tech sector?

Our Pillar II and III equity funds follow these exact same principles. Along with other equity pension funds, they have delivered the best returns for savers over the last 2, 3, and 5 years. (4)

Bank salesmen often warn that the weight of the US and the tech sector in index funds is too high, suggesting you should instead keep your money in the bank’s high-fee, actively managed funds. This is a common concern, but let’s look at the facts.

First, companies traded on US stock markets don’t just operate there. For example, while Apple and Coca-Cola are headquartered in the US, they sell products worldwide. Revenue earned within the US accounts for only about 40% of their turnover; 60% is generated elsewhere.

The same applies to the tech sector. While these companies develop new technologies and are categorized as “tech,” they earn a large portion of their revenue in other sectors like retail, manufacturing, or transport.

Second, the market is self-correcting. We haven’t “decided” to favor the US or tech; we are simply reflecting the state of the global stock market. Stock weights in our fund are based on their market capitalization. US-listed stocks make up 60% of the fund because that is currently the US share of the global market.

If India or China rises tomorrow and their companies grow larger than those in the US, the fund’s composition will adjust automatically.

Summary: Simple, logical, and low-cost

The core of the Tuleva Additional Investment Fund is simple:

We invest in the world’s most successful companies.

We bundle them into one portfolio (diversifying risk across 2,500+ firms).

We keep costs low so that the returns stay with you, not the middleman.

A careful observer might remember that a few years ago, the MSCI ACWI index included nearly 3,000 companies. Today, it’s around 2,500 because the index provider aims to cover 85% of the total value of all global listed companies using the largest players.

If you’re interested, take a look at this video, which provides an overview of how the market capitalization of the world’s largest publicly traded companies has shifted between 1979 and 2021.

The Additional Investment Fund portfolio must include instruments from at least six different providers because it is a UCITS fund. These regulations state that securities issued by a single entity can make up no more than 20% of the fund’s assets. This differs from pension funds, where the diversification rule applies at the fund level (up to 30% per fund), which is why our Second and Third Pillar portfolios consist solely of BlackRock sub-funds.

Tuleva fees drop again

The more people save at Tuleva, the less we all pay in fees. The less we pay in fees, the more of the returns we keep for ourselves. This is the essence of Tuleva’s model. Our assets under management have grown by 300 million euros in a year and exceeded the 1.3 billion euro mark. Therefore, we can lower fund fees once again. Starting December 1, the ongoing fees for all Tuleva funds will be 0.29%.

A year ago, Tuleva’s assets under management crossed the one billion euro threshold. It took us nine years to reach that milestone. In the last year alone, our assets have grown by over 300 million euros, bringing our total volume to over 1.3 billion euros. Together we paid 160 million euros into the funds. New savers brought us 70 million euros of assets previously accumulated elsewhere. The stock markets also had a good year, despite a crash in March.

We lower fees as soon as possible

Investing is a volume-based business, and as the assets under our management grow, the costs per investor decrease. Every new euro added to Tuleva funds helps reduce fees for everyone.

Tuleva’s model follows the principle set out by Jack Bogle, the founder of index funds.

In the last months, we have also made an effort to keep our costs under control. In August, we decided to conduct a larger part of our product development in sprints. This decision allowed us to reduce Tuleva’s permanent team by four people and consequently lower our running expenses.

For these reasons, we are able to reduce our fees, while still leaving ourselves adequate buffer to weather potential market downturns. Starting December 1, 2025, we are reducing fees across all Tuleva funds to 0.29%.

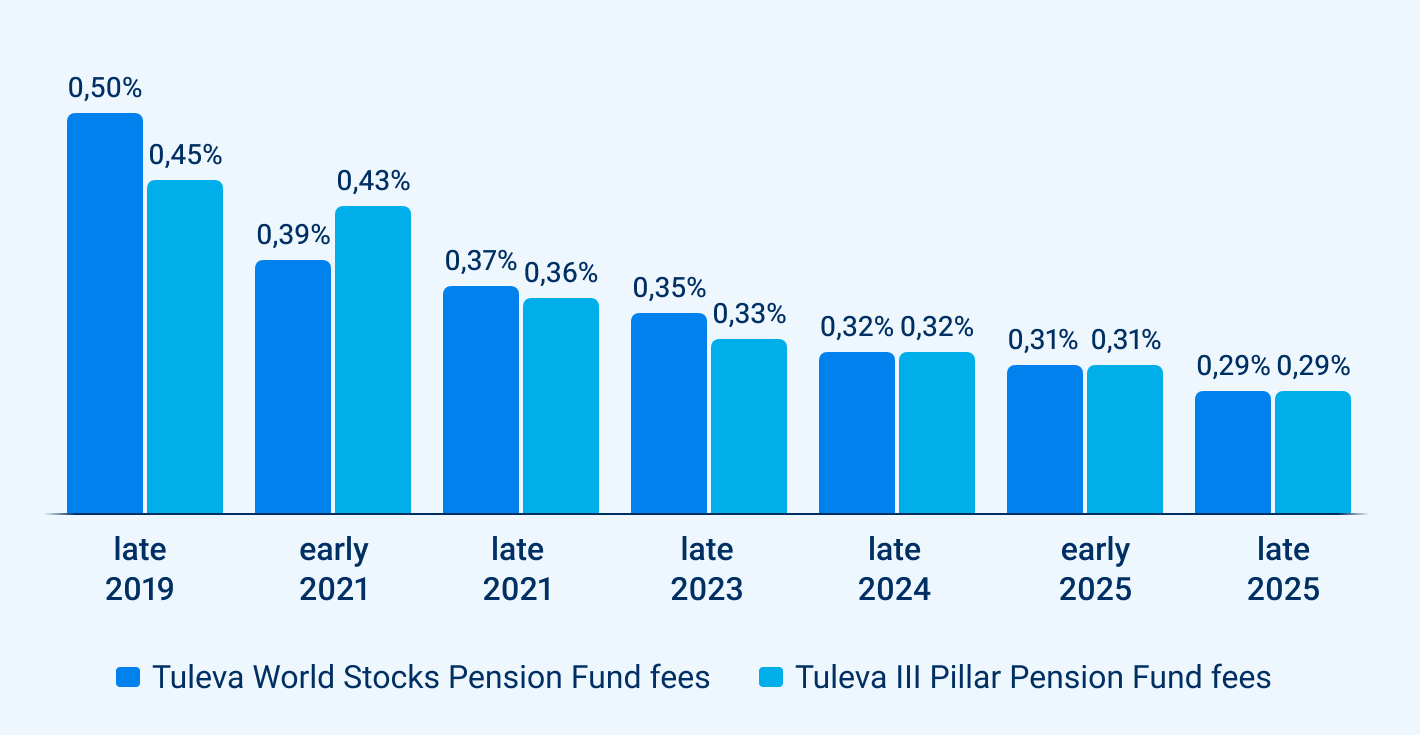

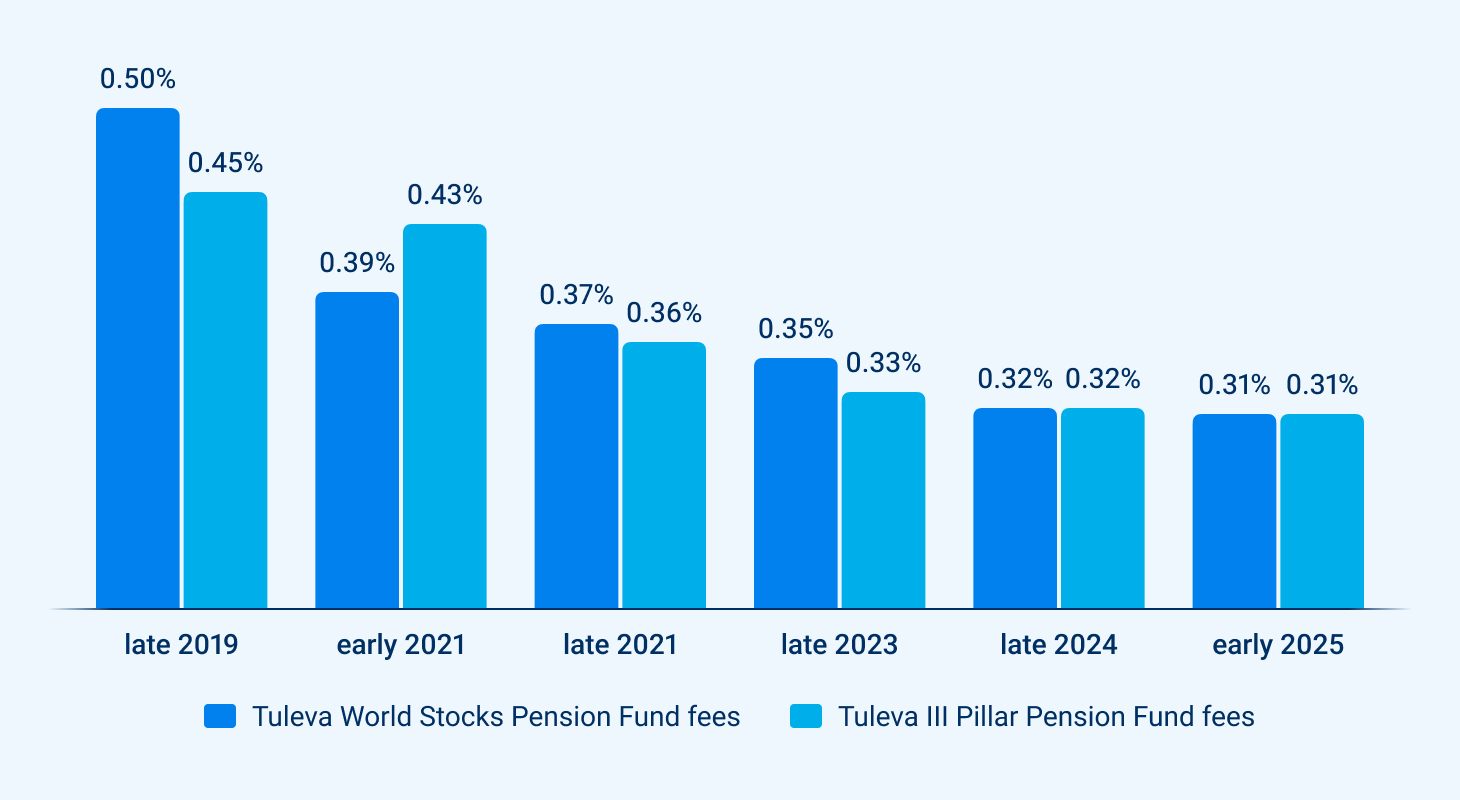

The chart below illustrates the downward trend in fees for Tuleva’s two largest funds.

Tuleva members benefit further because we return a portion of our fees to ourselves. Each year, every member receives a 0.05% rebate of the value of their savings in Tuleva’s second and third pillar funds.

The more people save together with us, the more confidently fees will drop for all Estonian pension savers

Lowering fees has a small impact on the average Tuleva saver, as fees decrease by only a few percentage points. However, that is not the main priority. Tuleva was created to increase competition among pension funds. We lower fees to make saving for retirement more affordable for everyone.

Lowering our fees does not make any single Tuleva fund the cheapest on the market. However, we are confident that all of our funds are good funds, as Tuleva remains the fund manager with the lowest average fees in Estonia by a significant margin. (2)

In the Tuleva model, everyone covers their own costs – no one else pays for your savings, and you don’t pay for someone else’s. In contrast, banks offer both low-fee funds and very high-fee funds, with the latter subsidizing the low-cost options.

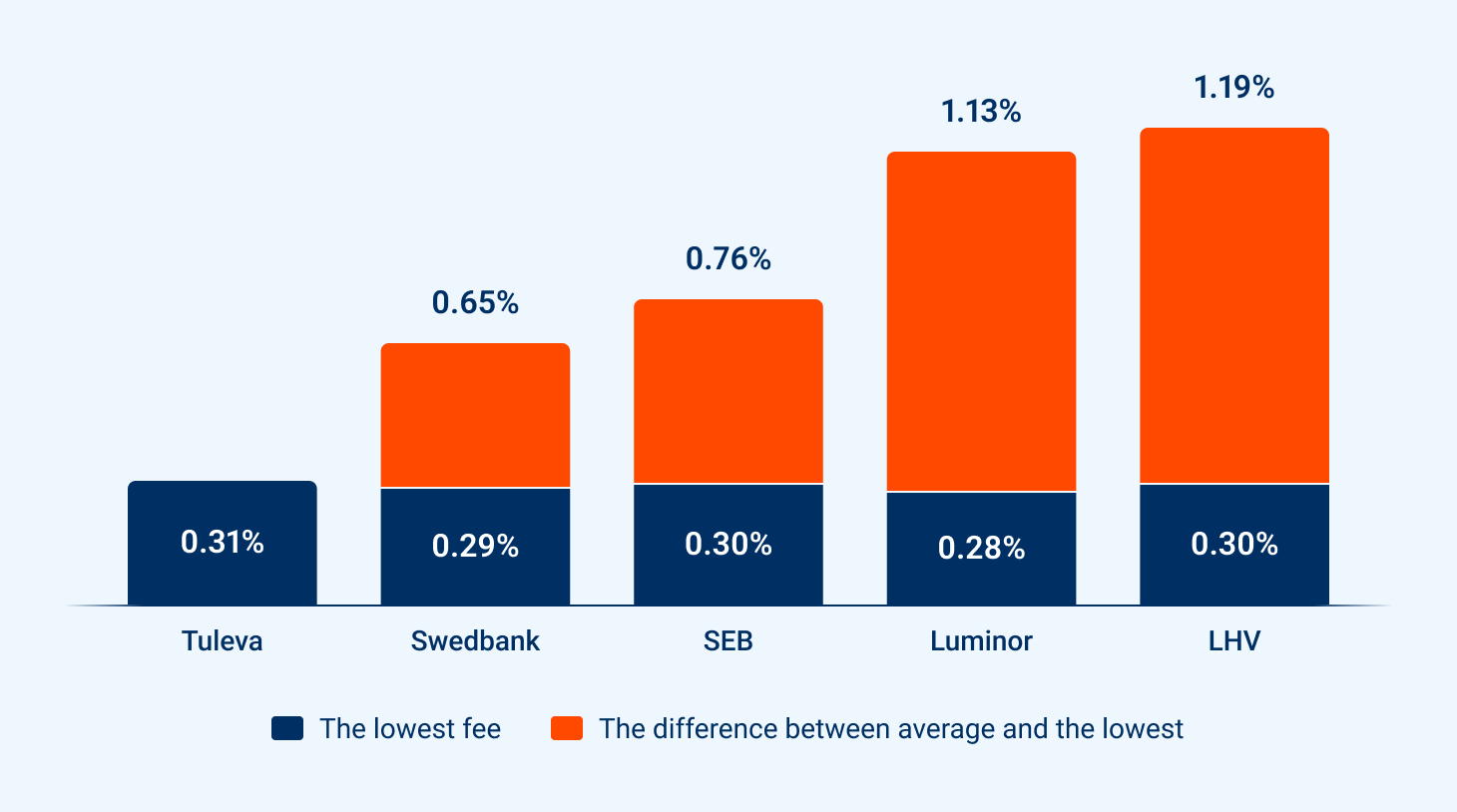

The chart below shows the asset-weighted average ongoing fees of II pillar pension funds at pension fund managers as of 27th Nov 2025.

The less you pay in fees, the more you keep yourself

While pension fund fees may seem negligible, their impact over the long term is significant. Tuleva investors understand that saving on fees means having more wealth in the future.

One in five people who recently transferred their second pillar to Tuleva previously saved in a fund with a fee over 1.2%. On average, those transferring from such a fund had accumulated €14,500 in their second pillar. In 2025, they would pay a fee of 1.2%, amounting to nearly €175. By moving their pension savings to Tuleva, they would instead pay just €45 – almost 4 times less.

This is not some distant future projection or theoretical figure; it’s real savings. It’s like switching your family’s expensive mobile plans to more affordable ones – a small effort that saves money and generates returns for decades. You can calculate the impact of fees on your savings using our pension calculator.

Tuleva lowers fees because we can

We are not pressured by the government or competitors to lower fees. The owners of Tuleva are the same people growing their wealth in our funds, and it is in their interest to keep costs under control. Thanks to this, other Tuleva investors can also rest assured that saving with Tuleva will become even more affordable in the future. As more people save in our funds, we can continue lowering fees. The larger our fund size, the lower the costs for everyone.

The chart displays the expenses and operating profit of all fund managers regarding the second pillar in 2024. At Tuleva, we keep costs as low as possible. The chart is limited to the second pillar because fund managers are not required to disclose similar data regarding the third pillar.Sources: Mandatory pension fund reports from fund managers’ 2024 annual reports; Tuleva’s calculations.

Initially, Tuleva’s goal was to bring low-cost index funds to Estonia. Now we know that our greatest contribution is helping more people save wisely and consistently. That’s why we aim to cut through the noise and misleading advertisements to help people make informed decisions.

Moreover, the larger we grow, the stronger our voice in advocating for investors. Every euro saved strengthens our ability to push for a fair and modern pension system in Estonia.

See how much you’re paying in fees on your pension savings.

We made the terms of our pension funds more precise

We updated the terms of our pillar II and pillar III funds. The goal of these changes is to bring the terms fully in line with our investment strategy and clarify some unclear wording. The portfolios themselves are not changing.

Tuleva’s fund terms differ from most other Estonian pension funds in one important way: while fund terms usually state what the fund manager may do with savers’ money, ours state what we do. This way, reading our fund terms gives a clear overview of what assets are actually in the portfolio. (1)

Changes in investment restrictions

Compared to eight years ago, when we started Tuleva, more low-cost index funds have become available to us as a fund manager. For example, just 4–5 years ago, we couldn’t include Exchange Traded Funds (ETFs) in our portfolio because their costs were too high. Today, those costs have dropped. As a result, around one third of our stocks fund portfolio is now invested through ETFs. The rest is invested in low-cost traditional index funds, which – unlike ETFs – are not listed or traded on any stock exchange, just like Tuleva’s pension funds.

As we analysed the terms, we realised they didn’t fully reflect our investment strategy in every detail as we had originally planned. That’s why we clarified the wording and aligned the updates with the Financial Supervision Authority. Our investment strategy remains the same. So, what exactly has changed?

One of the key principles we follow when selecting funds for our portfolio is that we only buy and sell fund units in euros. This keeps transaction costs lower.

Previously, the terms required that fund units must be denominated in euros – meaning the fund’s NAV, performance and costs are calculated in euros. But for an index investor, this doesn’t really matter, since internal accounting has no impact on a fund’s performance or risk. Any fund that invests outside the euro area is exposed to currency risk anyway, because the underlying assets (like company shares) are bought in USD or another local currency. That’s why we clarified the terms: funds in our portfolio must be tradeable in euros.

Another principle we follow is daily liquidity. Our funds must be able to sell their investments quickly. Previously, the terms stated that fund units in our portfolio must be traded on a regulated securities market. But that’s not the only way to ensure daily liquidity. The index funds we hold in our portfolios – even though some of them are not Exchange-Traded Funds – allow us to redeem our units within a few day. That’s why we revised this wording in the terms.

Update to the fund manager’s capital requirement

We also brought the fund terms into line with a change in the law that sets how much of its own money the fund manager must hold in pillar II funds. When we started Tuleva, the requirement was 2% of the fund’s assets. A few years ago, the government lowered it to 0.5%.

Why don’t we set a higher requirement for ourselves? We don’t need to. Most of the money in Tuleva’s pension funds already belongs to the owners of the fund manager – the members of the Tuleva Commercial Association. In addition, the majority of our association’s capital is invested in our own pension funds – as stated in our membership capital terms. That’s why no extra obligation is necessary. (2)

When do the updated terms take effect?

Under the law, changes to fund terms only come into force after unit-holders have had time to review them and, if they wish, leave the fund at no cost. That means:

The updated terms of the Tuleva World Stocks Pension Fund and the Tuleva World Bonds Pension Fund will take effect on 1 September 2025.

The updated terms of the Tuleva Third Pillar Pension Fund will take effect on 15 June 2025. (3)

Tuleva never charges entry or exit fees. This means you can leave our funds at any time without paying a redemption fee. If you wish to transfer your savings elsewhere before the new terms take effect, please submit your application by: 31 July 2025 for pillar II funds (Tuleva World Stocks Pension Fund and Tuleva World Bonds Pension Fund); 14 June 2025 for the pillar III fund (Tuleva Third Pillar Pension Fund). You can submit your application through your internet bank, at the Pension Centre, or on Tuleva’s website.

As of the end of April, our fund manager’s own investment represented 1% of the pillar II fund assets.

Under the law, pillar II fund terms can take effect on the next switching day (which is 1.09.2025), and pillar III terms one month after notice is published.

Fees drop again, and clearer recommendation to invest in an equity fund

We implemented two positive changes in our funds. First, we lowered fees once again — now, the ongoing fees for all Tuleva funds are just 0.31%. Second, we clarified our recommendation to save in an equity fund regardless of age. The goal remains the same: to create the best conditions for growing our money as savers.

The more savers in Tuleva, the lower the fees for everyone

Since the launch of Tuleva, we have lowered our fees six times. Back in 2017, we started with a 0.5% fee, and now, as of March, the total ongoing fees for both the second and third pillar funds have dropped to 0.31%.

Investing is a scale business — the larger the assets we manage, the lower the costs per saver. Since our last fee reduction in November, our funds have grown by €100 million, allowing us to lower fees again.

The chart below illustrates the downward trend in fees for Tuleva’s two largest funds.

I’m confident that we’ll reduce fees even further in the future. After all, Tuleva is owned by its savers, and we have every reason to lower costs as soon as it’s sustainable.

For Tuleva association members, saving in our funds is even more beneficial. As owners, we get part of the fee back — every year, we receive a 0.05% member bonus on our second and third pillar savings in Tuleva funds.

For those who are not members of Tuleva association, you can find some slightly lower-fee index funds in the pension fund selection at banks. These are also solid options for long-term saving. We’re genuinely happy that index fund fees across the board have significantly decreased over the last five years.

It’s only sad that the fees for banks’ old actively managed funds have not followed the same trend. In fact, nearly two-thirds of Estonia’s second-pillar savers are still in those expensive funds. The reality is that banks cover their high costs and generate profits for their owners at the expense of these savers.

The chart below shows the asset-weighted average ongoing fees of II pillar pension funds by pension fund managers as of 3th March 2025.

Money should generate returns for as long as possibleIn addition to lowering fees, we also clarified our recommendation to stay in an equity fund regardless of age. Previously, we set a conditional age limit at 55, while still outlining cases where stock funds could be considered beyond that. We’ve learned that our recommendation needs to be even clearer.

So, here it is: A low-cost equity fund is the best choice if you don’t plan to withdraw your entire second pillar within the next five years.

The key point is that the biggest risk for Estonians when saving for retirement isn’t market fluctuations — it’s not saving enough. Very few of us earn high enough salaries to accumulate a sufficient amount without earning returns on our savings.

Risk and return go hand in hand in investing. While stock prices fluctuate more than bonds, the historical long-term returns of stocks have been significantly higher. Finnish and Swedish pensioners don’t live well because their governments hand out generous benefits, but because their savings have compounded strong returns over decades.

What should you do?

Market fluctuations won’t worry us as savers if we use our second and third pillar funds as a regular pension supplement. The state pension (first pillar) provides stability. That’s why Sweden, for example, automatically keeps people saving in equity funds even at an older age — because it serves as an addition to their national pension. In Sweden, people can’t even withdraw their pension savings in a lump sum; they can only take it as monthly payments.

What Sweden has made automatic for its citizens, we can choose to do manually. The good news? You don’t have to do much at all. Tuleva savers can confidently continue accumulating money in our second and third pillar stock funds until retirement without unnecessary fund switches.

If you eventually need to start using some of your savings, just log in to our website and set up regular drawdowns (by signing a fund pension agreement).

Historical stock market data suggests that with this approach, there’s less than a 2% chance that your total withdrawals will be lower than your total contributions — even if you moved your savings into stock fund just before starting withdrawals.

Of course, this is not a guarantee — the future may look very different from the past 100 years in the stock market. It’s human nature to underestimate long-term statistical probabilities. But looking at it the other way around, this is how we can make the most of the contributions we’ve made over our lifetime.

The updated fund prospectuses, along with official explanations, are linked here: II Pillar Prospectus and III Pillar Prospectus (in Estonian). These took effect on March 3, 2025.

(1) Over the past five years, fees for all Estonian second-pillar index funds have decreased by 10–20%. Meanwhile, fees for actively managed funds have mostly increased. You can see the fee trends here.

(2) Finland’s largest pension fund manager, Ilmarinen, has achieved an average annual return of 6% over the past 27 years, while Sweden’s national pension fund, AP7, has delivered an average annual return of 9% over 23 years. Sources: Ilmarinen 2024 annual report and AP7 Safa website.

(3) More specifically, historical data suggests that with 95% certainty, a person who moves their savings into an equity fund at age 55 will see their assets exceed both their starting balance and interim contributions after 10 years. For those interested in statistical analysis, this Google Sheet provides further details. I’ve kept the calculations as simple as possible.

How do we use membership fees?

Membership fees are used to develop the Association and to represent the interests of members. The fees of our first members were used to raise the fund’s initial capital, introduce Tuleva to the general public, and make preparations to start the fund, including application for an activity license from the Financial Inspectorate. From this point forward, membership fees will be used for the following activities:

Membership community management and communication

Development of Tuleva’s web page, blog, and other informational channels

The creation of proposals and influence analysis to improve the Estonian pension system, in cooperation with the Ministry of Finance and other state organizations

Development of Tuleva’s IT systems

Preparation and analysis of voluntary savings products and Third Pillar options

Your joining fee helps to bring well thought ideas with big impact to decision-makers.

Every euro saved gives a Swede almost a third higher pension than the same amount saved by Estonians. Estonia needs a smarter and measurable pension strategy.

As the first and only association representing pension savers, Tuleva is a credible partner for Ministry of Finance and state legislative bodies. We participate in pension strategy discussions, where next to the officials only banks and insurance companies used to be represented.

We help to make better laws. The laws that protect the people. The laws that maximize our profits from our, not banks’ savings.

We have our first achievements. For example

On Tuleva’s initiative, people in Estonia saved only during last year 1.5 million euros, because the fund managers are no longer allowed to charge high fees for changing the pension fund.

We sent a petition to parliament, signed by 2300 people, that proposes to reform how people can use their II pillar savings.

We do not organise demonstrations or spread random complaints. We are direct, we analyse issues and offer constructive solutions.

Tuleva is a social company with a goal to earn profit for its members.

Tuleva’s main principle is that people themselves save money for their future, using contemporary technologies and bypassing unnecessary middlemen and costs as much as possible.

Every year, each member who has transferred their second or third pillar to Tuleva pension funds, earns a member bonus. Member bonus is very small at first, but it will grow together with member’s pension assets. Bonus is transferred to your personal capital account at Tuleva. This is your ownership stake in Tuleva capital and this stake can earn you additional profit.

When Tuleva grows, our funds under management grow and we add new products to our offering, then the association will earn profit. The profit is then divided among members, as set in our Articles of Association.

As always with profit from entrepreneurship – this depends how well our venture is doing. The founders are convinced, that the 125-euro joining fee pays for itself many times over. But we do not give promises.

How is member bonus calculated?

At the end of each year

We calculate how many pension fund units each member had on average during the year in euros

Multiply this by 0,05% and transfer the resulting amount to member’s capital account

Every 5 years, members annual meeting decides whether to pay our accumulated profit as a dividend or keep it invested.

Tuleva is for people who care.

Every member has a vote on annual general meeting and has a right to elect and be elected to Tuleva’s board of directors and other supervisory bodies. This is the official part and it is very important.

Every day we share our ideas and experience among Tuleva members in our Facebook group, e-mail, phone and working groups. Among our community, there are people who care about the society and have very different skills. Many are ready to take responsibility for ensuring us a better future.

Tuleva team listens very carefully to our members and uses their ideas for making Tuleva better. We are only starting and believe that the power of thousands of smart people can be used for increasing our common good.

How does the calculator work?

Tax benefit is simple: the government pays you back the income tax on your third pillar contributions. Tax benefit applies to contributions that do not exceed 15% of your gross income or 6000 euros, whichever is smaller.

Your maximum contribution amount to third pillar is thus 15% x gross annual income. If your annual income is over 3333 euros per month (gross), then you can contribute to third pillar 6000 euros.

Tax benefit equals 20% x your third pillar contributions.

NB! Your tax benefit cannot be bigger than the income tax you have paid during the year. Thus: if your gross income is less than 614 euros a month, then your maximum contribution is less than 15% of your income. More precisely – your maximum contribution per month is then: gross monthly income x 0.964 – 500.

With less than 519 euro monthly income you are not paying income tax most likely and hence you do not have any tax benefit in contributing to third pillar.

Check the e-tax board to see how much gross income you have received this year

In the menu on the left, select Registers and inquiries -> My income. You can see the gross income earned this year on the basis of the data that payers have submitted to the tax office to date. Check whether income tax has been withheld from the payment amount or not, according to the payer. To do this, click on the name of the person making the payment, and in the last column of the summary information, you will see information about the withheld income tax.

NB! It is possible that your employer(s) have not yet declared the salary data for the last month(s) of the year. You can check this by clicking on the name of each payer.

If you know that income is still coming to your account this year, add it yourself.

Please note that all income that reaches your account this year will be included in the calculation for this year (if the December salary is received in January, it will be included in the next year’s income calculation).

You can also add income that you plan to declare in the income tax return this year: rental income, interest paid by crowdfunding portals, income from the transfer of securities or other property.

Don’t worry if you don’t know the exact amount of your annual gross income today. Calculate the approximate amount and then find the optimal third pillar money placement with the calculator. If the actual annual income turns out to be higher than expected, your contribution will simply be slightly below the income tax allowance limit. Nothing terrible will happen even if you put a little more than the tax credit limit in the third pillar. The law does not prohibit it – if you exceed the limit, you simply cannot get the income tax back.