-

Tuleva management report for first half of 2023

If you have just a 1 minute to read: Since the beginning of the year, world stock markets and the prices of Tuleva’s World Stocks Pension Fund and Tuleva’s Third Pillar Pension Fund units have increased by 15%. Over the past five years, the price of a unit in Tuleva’s World Stocks Pension Fund has…

-

How to talk about pension fund performance?

Performance is the buzzword of pension fund marketing. Swedbank writes: “The bar is high. And fees low.” LHV claims to be the only one to increase the value of funds since early 2022. And Tuleva says its “performance will never lag far behind the average of the world securities markets”. How do you know who…

-

[Updated in 2026] How to make the most of your third pillar pension?

The third pillar is an excellent way to save for your future. It offers a simple and automatic investment option where you can invest your money in broad-based index funds. In addition, the Estonian state provides support through an income tax rebate on the amount you save. Thanks to the tax rebate, the third pillar…

-

Wise added to Tuleva’s portfolio

In May, MSCI, the world’s largest compiler of stock market indexes, included the first Estonian company, Wise plc, in its global equity market indexes. As a result, Wise shares were added to our pension fund portfolio. Interestingly, just a few months earlier, MSCI had removed Western Union, a company operating in a similar sector but…

-

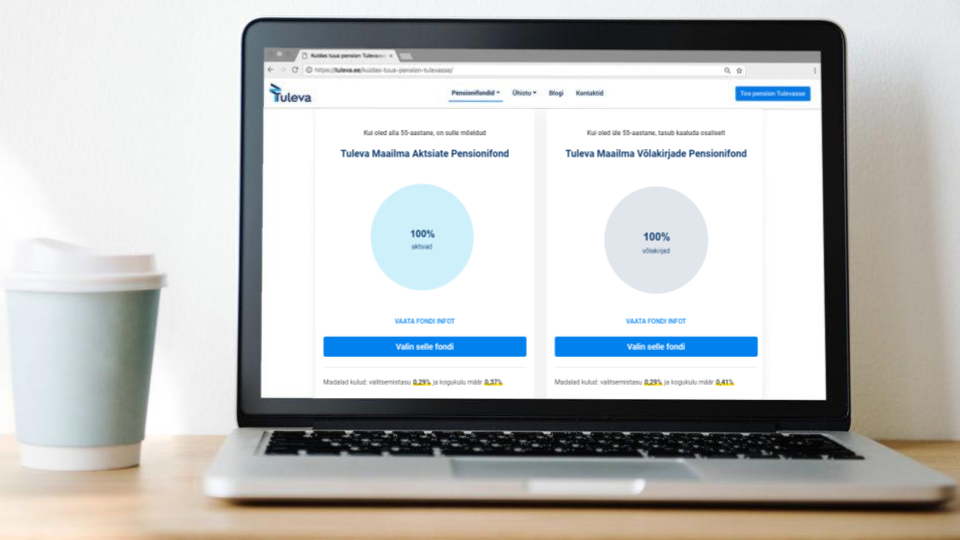

[Updated 2025] Tuleva pension funds: where do we invest and which fund is right for you?

In spring 2016, 22 Estonian entrepreneurs and prominent public figures made a promise to one other to help make pension saving more cost-effective for people in Estonia. We established Tuleva. The birth of better pension funds was made possible by the 3,000 Tuleva members who teamed up with the founders right from the first months. Today, the dream is…

-

Tuleva management report 2022

Dear Tuleva members and investors, The past year was hectic. Inflation reached the highest level seen in recent decades. A war was started in Ukraine. World stock markets fell by nearly 15%. As you know, when saving with Tuleva, we set aside a piece of our salaries every month and use it to buy more…

-

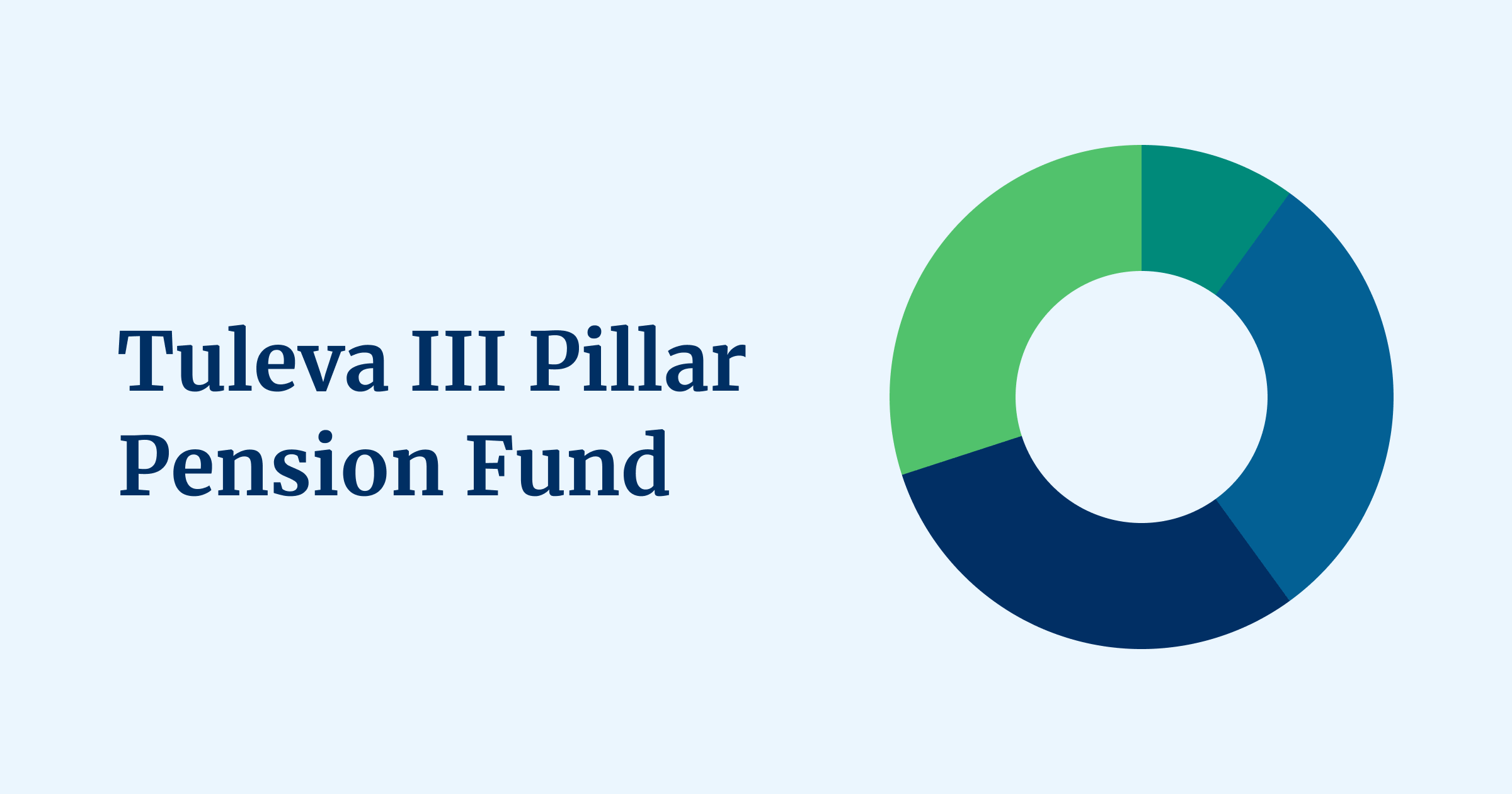

[Updated in 2025] What is inside Tuleva III Pillar Pension Fund?

To date, we have been able to save money in Tuleva’s very own third pillar fund more than three years! As in our second pillar funds, you don’t have to be a member of the association to join us in the Tuleva third pillar. Start investing from the third pillar! A simple rule to follow…

-

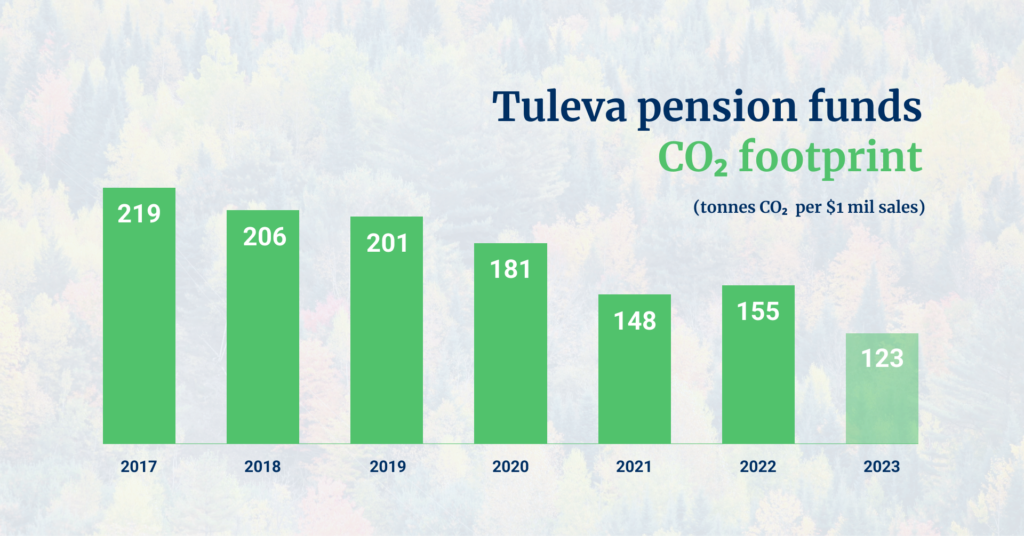

Tuleva funds will implement sustainability policy from the autumn

Tuleva pension funds will follow the principles of environmental sustainability and social responsibility, excluding investments in companies that do not meet the relevant criteria. Rather than creating an additional small “green fund”, Tuleva will make its large funds more sustainable. In exactly the same way as we don’t have a single good pension fund hidden…

-

The second pillar is your asset: How to get the most benefit from It?

Kristi Saare and Tõnu Pekk have helped cut through the clutter of information about pension pillar reforms. Below you’ll find a summary that outlines how to withdraw from the second pillar and how to maximize its benefits. The second pillar is truly your asset While the second pillar was always legally your own, many didn’t…

How do we use membership fees?

Membership fees are used to develop the Association and to represent the interests of members. The fees of our first members were used to raise the fund’s initial capital, introduce Tuleva to the general public, and make preparations to start the fund, including application for an activity license from the Financial Inspectorate. From this point forward, membership fees will be used for the following activities:

- Membership community management and communication

- Development of Tuleva’s web page, blog, and other informational channels

- The creation of proposals and influence analysis to improve the Estonian pension system, in cooperation with the Ministry of Finance and other state organizations

- Development of Tuleva’s IT systems

- Preparation and analysis of voluntary savings products and Third Pillar options